When the Boardroom Door Swings

General advice only — prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

Dear Reader,

A director resigning is one of the dullest announcements in the ASX feed.

The cessation notice. The polite paragraph about pursuing other interests. The chairman’s thanks.

Most investors scroll past. Most of the time, that’s the right move.

Not always.

Every now and then, the same notice lands twice on the same ticker inside a fortnight. Two directors gone, sometimes three, often without a story tying them together.

Let’s call these a ‘cluster’. We’ll define a cluster as when two or more directors leave the same company within 90 days.

We’ve pulled 687 of these from the last five years on the ASX. About 137 a year, against a universe of roughly 1,800 listed names.

This deep dive explores the relationship between ASX boardroom departures and stock performance in recent years.

We’ll highlight the companies that our model predicts will see big gains and losses right now. But before that, let’s dig into the relationships that the data has uncovered.

More resignation letters don’t mean more pain

Imagine you’re walking past a building and hear the fire alarm go off. Is there a fire inside, or is it just a test?

Now imagine there’s smoke billowing out the windows and people stampeding for the exits.

Is there a fire?

The smoke and the people fleeing at a pace are a strong indicator that there’s a fire inside.

Most people would assume the same logic holds for boardroom resignations. The faster the stampede for the door, the more problems are likely to unfold in the coming months.

But it’s not so straightforward.

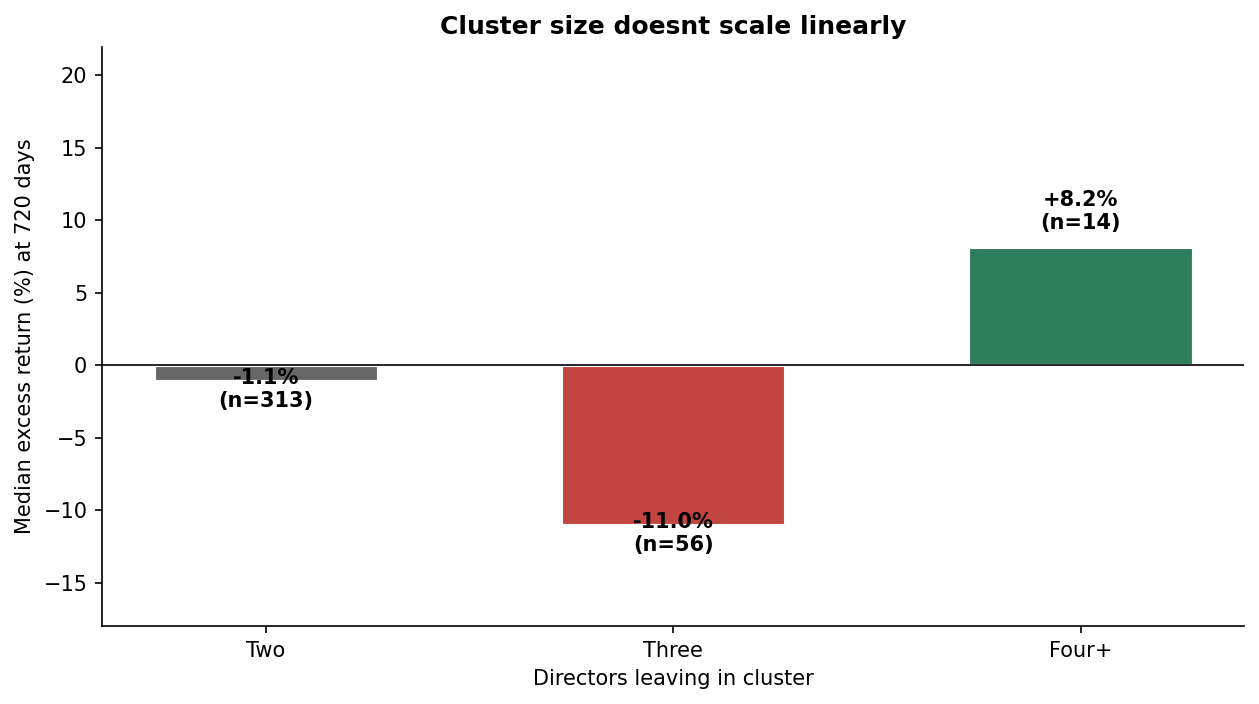

Cluster size at 720 days (Source: TheMarketsIQ.com / ASX Announcements)

Two-director clusters are the bulk of the dataset, and they roughly track the size-matched control over two years. Median excess return of -1.1%.

A minor underperformance.

Three-director clusters are felt late. -4.7% at twelve months, then the gap widens to -11.0% by twenty-four. The damage takes time to land.

Four-director clusters break the pattern. The median is positive, +8.2% at two years.

Strange.

But a deeper look reveals an interesting dynamic.

Tabcorp’s 2022 demerger. Cuscal’s 2021 demutualisation. Star Entertainment’s AML-driven board purge. Abacus Group’s restructure.

When four people leave the boardroom within 90 days, it’s often corporate action. A takeover, a demerger, a regulatory reset. The price reflects whatever’s driving the action, not the directors leaving.

And boards rarely get flushed for a stellar performance.

But that’s not all. The number of directors isn’t the whole story.

The seat being vacated tells us a lot as well.

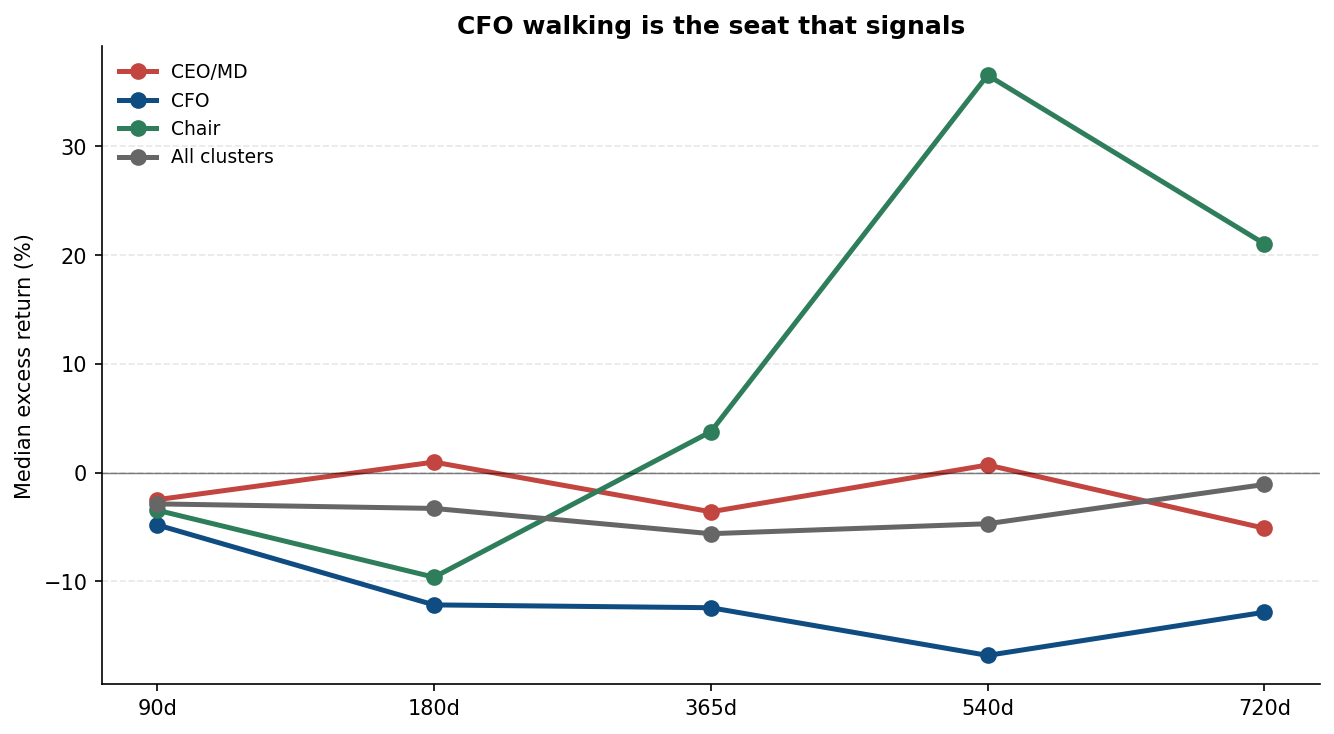

The seat that signals isn’t the one you’d expect

The senior-role read inverts the headline.

Role x horizon (Source: TheMarketsIQ.com / ASX Announcements)

CEO and managing director departures look loud and read quiet. Forty-two clusters across the dataset, with a 365-day median excess return of -3.6%. Close to the all-cluster median.

CEO walks make headlines. They don’t predict performance.

The real signal is the CFO.

Twenty-nine clusters with a chief financial officer involved. Median 365-day excess return of -12.4%, drifting to -16.8% at eighteen months before steadying around -12.9% at two years. The cleanest senior-role cohort the dataset produces.

The CFO is the most credible witness on the balance sheet. When the witness walks, the implications take quarters to land in the public numbers, and the market reacts late.

The chair line runs the other way.

The chair-involved cohort drops to -9.6% at six months, then climbs back. By eighteen months, it’s +36.6% above its size-matched control, settling near +21% at two years.

The chair leaving can be a sign of positive change.

The CEO walking is, for forecasting purposes, almost interchangeable with any other director walking. The CFO leaving in a cluster is the year-two warning sign.

Holding time also plays a role.

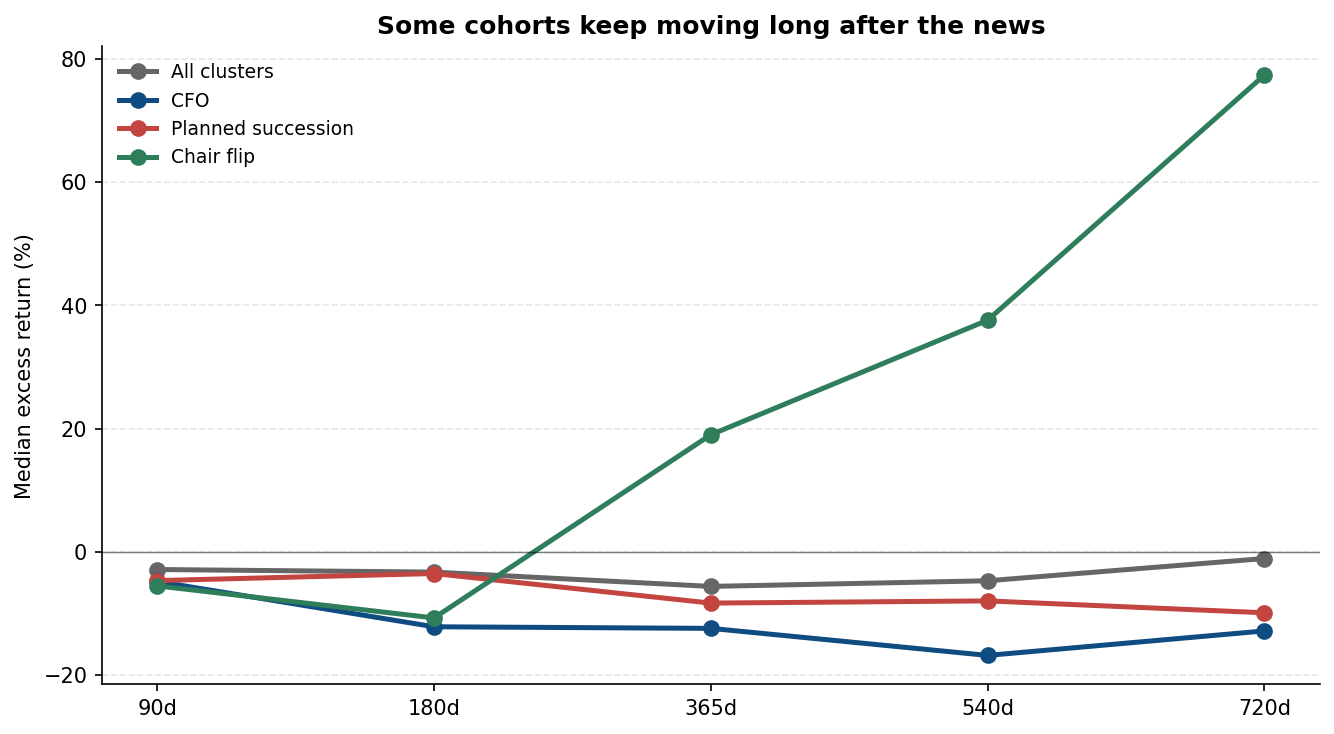

Some cohorts keep moving long after the news

The change over time is most pronounced when the chair is involved.

Cohorts pulling away (Source: TheMarketsIQ.com / ASX Announcements)

The all-cluster line is hardly explosive. -3% at six months, -6% at twelve, -5% at eighteen, -1% at twenty-four. Most damage comes early. The universe roughly stabilises.

The interesting lines are the cohorts that pull away.

CFO clusters keep breaking. A staircase down through eighteen months before a slow reversal. The financial officer’s exit takes quarters to surface in the public numbers, and reality keeps rolling out.

Planned succession is the slow bleed. -3% at six months, -8% at twelve, -8% at eighteen, -10% at twenty-four. The intuition is that a successor named inside thirty days reads as orderly. A safe version of a cluster.

The data says the opposite. By two years, the ‘planned’ bucket is the only major cohort still drifting south, while the all-cluster median has come back to flat.

The chair-involved cohort is the cleanest example.

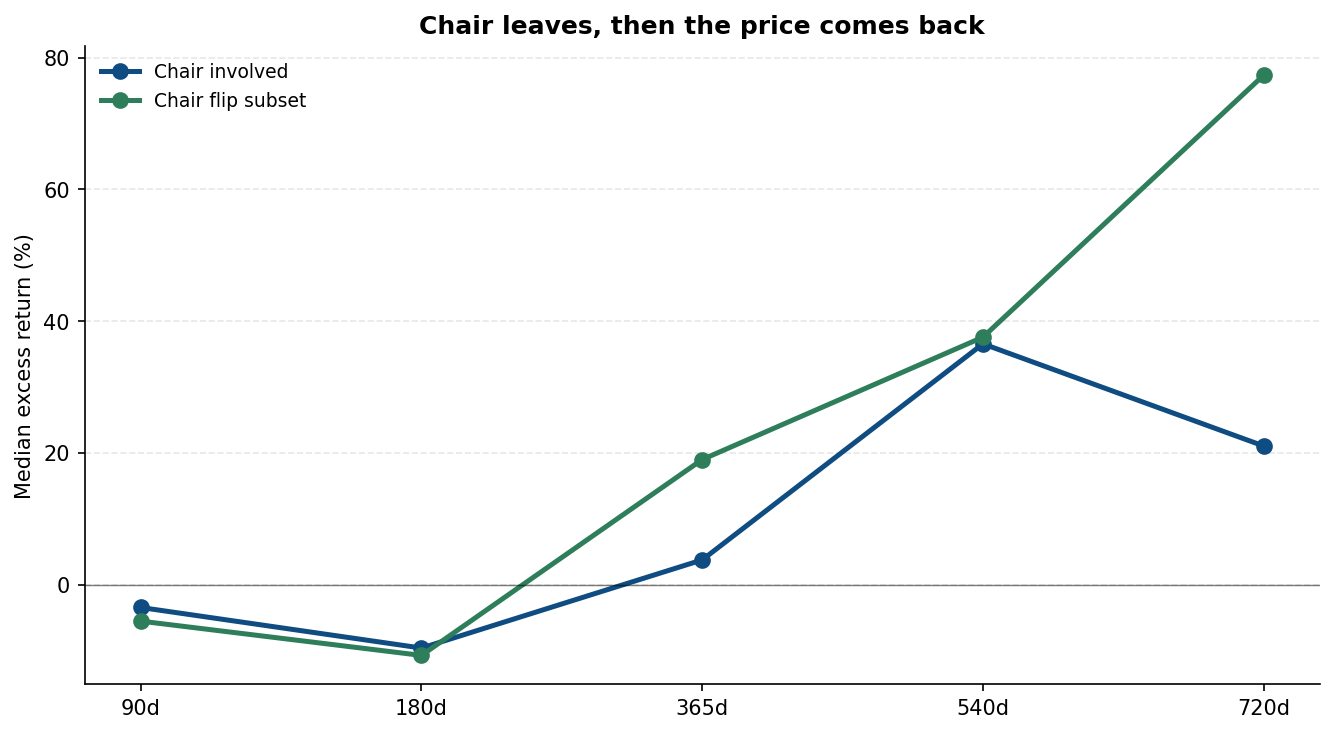

Chair leaves, and the worst time to act is six months in

The chair-involved cohort traces a U.

Chair arc (Source: TheMarketsIQ.com / ASX Announcements)

The trough is at 180 days, -9.6%. Markets sell on the news, then sell again as the new chair makes their first uncomfortable decisions, and then the price settles.

By 18 months, the cohort is 36.6% higher than its size-matched control.

The chair-flip subset, where the next chair is named within thirty days, sharpens the arc. +19% at 12 months, +37.6% at 18, a tail running to +77.4% at two years on a small sample of nine.

The worst time to sell after a chair resignation is the first six months.

The cohort that recovers fastest is the one where the board has the next chair lined up. The cohort that suffers longest is the one where the chair walks with no successor named, and the search plays out in public.

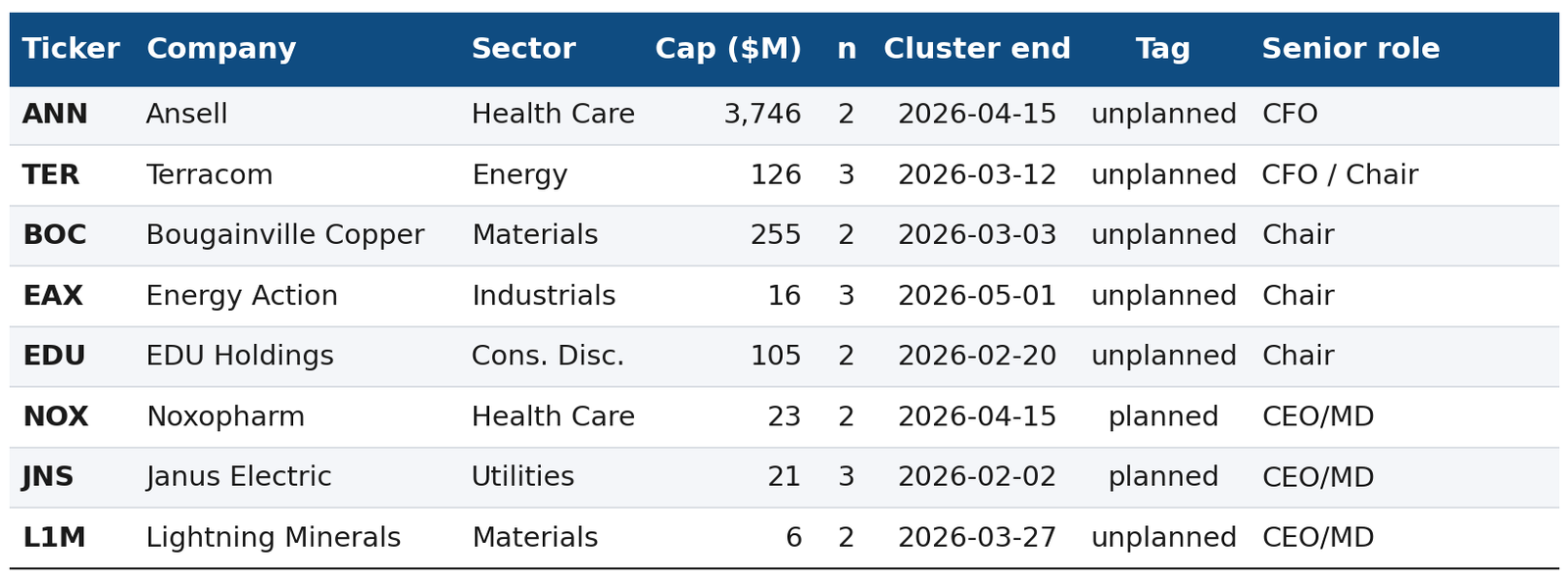

ASX stocks with boardroom departure clusters

Forty-seven clusters sit inside the last 120 days. Most are the everyday two-director bucket. The ones worth your attention are the senior-role-tagged subset.

The following table gives us the company, cluster size (n) and leadership role vacated.

Live screen archetypes (Source: TheMarketsIQ.com / ASX Announcements)

Ansell (ASX:ANN) is the cleanest. A $4.5 billion company, CFO-involved, unplanned. The same configuration that’s produced the cohort’s -16.8% median read at eighteen months.

Both Terracom (ASX:TER) entries sit in the CFO-and-Chair window. The same ticker has lost both senior officers in just five weeks.

Bougainville Copper (ASX:BOC) is in the chair-involved bucket where the U-curve says the worst weeks are the first 26.

The three CEO/MD-flagged names read the most dramatic at first glance. Noxopharm (ASX:NOX), Janus Electric (ASX:JNS), Lightning Minerals (ASX:L1M). They’re the ones that catch the eye. They aren’t where the data says the signal lives.

The case matters more than the cohort

Cohort medians describe averages across hundreds of names. They don’t describe the company in front of you.

Individual returns inside the cohort vary widely.

Two cohorts are worth paying attention to in this data. The chair and the CFO.

When the chair walks near another board departure, the price is likely to fall. The first six months are the worst, a trough around 180 days. After that, the cohort recovers.

When the CFO walks, expect the pain to endure. Six months is mild. Twelve months is worse. Eighteen months is when the cohort reaches its low, at -16.8% relative to a size-matched control.

We can gain small morsels of edge by looking back at historical data. But we need to keep in mind that the markets are always changing.

This isn’t an investment strategy. We hope it prompts further reflection and research for our readers.

Until next time, happy investing.

Izaac Ronay

Check out Explosive Growth for leading stock market research and The Week’s Edge for our ongoing take on the markets and investing.

Izaac is a broker and trader with Vitti Capital. He brings over 10 years of trading experience with top-tier global trading houses and 20 years of experience analysing and investing in ASX listed equities.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital — including the author of this report — may hold positions in the companies mentioned or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.