The Twenty-Year Supply Wave Hiding Inside the Budget

This article is for general information only and is not personal financial advice.

Dear Reader,

There was a big move signalled in the budget this week. It could be just the beginning of a complete overhaul of one of our most crucial industries.

While the country argues about negative gearing and capital gains, the Government has quietly rewired Australia’s gas market for the next twenty years.

The headlines missed it. Energy security has been such a hot theme it’s an almost unforgivable oversight.

The five-minute budget guides have it as a footnote. Most retail investors are pricing tax hikes and missing that the entire cost structure for Australia’s heavy industry just caught a structural shift.

The government loves to hide big news in plain sight, and this piece was no exception. It’s there in the budget, in black and white. But it’s suspiciously light on detail.

The headline change, however, is clear.

We’ll get into the big ASX winners, the losers, and a wildcard as we see it.

But first, let’s recap the actual change.

What the Budget Actually Said

Buried in Tuesday’s budget is a single legislative paragraph that does more for manufacturing than any tax cut.

From 1 July 2027, LNG exporters have to set aside 20% of any new export contract volume for the domestic market. It’s hardwired into legislation, not Ministerial discretion.

It supersedes the old Australian Domestic Gas Security Mechanism, the stick the Government has had since 2017 and never used. It replaces the voluntary Heads of Agreement that the Government and the three Gladstone exporters have renegotiated every few years since.

Existing export contracts are untouched. The 20% bites on new contracts only, as legacy offtake agreements roll off. So the policy starts quietly and ramps up over the next 15 to 20 years.

An excerpt from the budget lays it out.

‘The Government is introducing a domestic gas reservation so that LNG exporters supply a proportion of their total production to the domestic market, equivalent to 20 per cent of exports. This will secure additional supply of gas, drive downward pressure on prices for all users and build out domestic energy resilience in the face of volatile international markets.

The domestic reservation scheme will commence on 1 July 2027, with final consultation on legislation throughout June and July 2026.’

The wording is a bit obscure. The budget mentions ‘LNG exporters’ generally, but the agreements mentioned are east coast specific. So, we don’t yet know if WA and NT producers will be touched.

We’ll need to watch how the actual legislation plays out. Expect there to be frantic negotiations taking place in shadowy back rooms. Let’s assume for now that the East Coast market is the target.

That’s the mechanism. Now the math.

Quick refresher on the words

Natural gas is the raw stuff. It travels through pipelines to households, factories and power plants.

LNG is the same gas chilled to minus 161 degrees, condensed to liquid, and shipped on tankers. It packs 600 times more energy into a vessel than the gas state would.

When the budget reservation says ‘LNG exporters’, it might mean the three big Gladstone players. Shell’s QCLNG. Santos’s GLNG. Origin’s Australia Pacific LNG.

The reservation is on their gas. Pipeline-only producers selling direct to Aussie users were never going to export anyway, so they sit outside the rule.

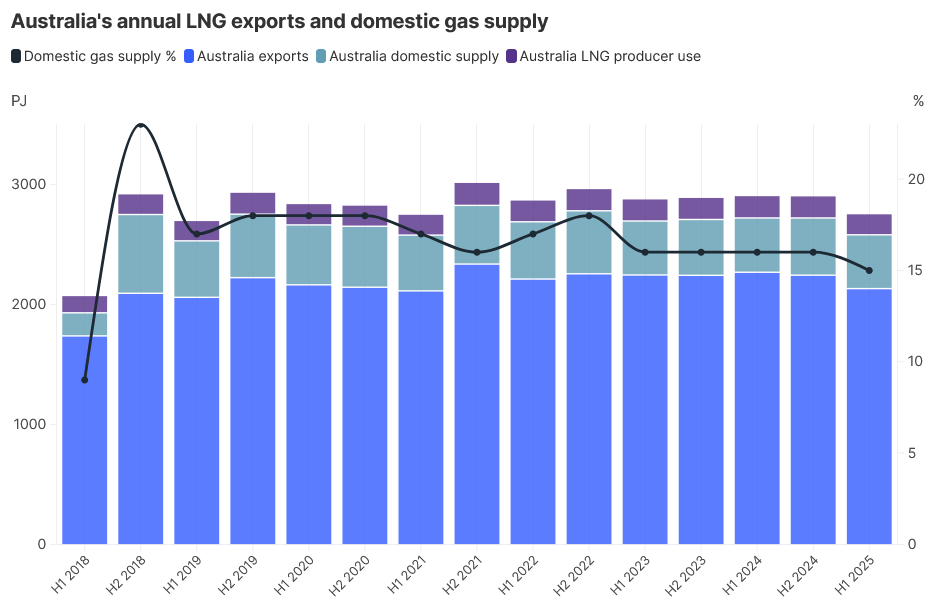

Across all of Australia (east coast and west coast combined), domestic gas users got only 15% of total Aussie gas supply in H1 2025. The rest left the country as LNG, with a slice of producer use taken off the top.

Australia’s annual LNG exports and domestic gas supply (Source: IEEFA)

Now zoom to the east coast on its own. AEMO’s H1 2025 numbers put domestic at 25% of east coast production and LNG export at 75%. That east coast number is the one the reservation policy targets.

Run the steady-state math.

East coast Australia produces about 2,000 PJ of gas a year. 500 PJ stays home today. The other 1,400 PJ gets liquefied at Curtis Island and shipped to Japan, China and Korea.

If every legacy export contract rolls over onto the new 20% rules, then 20% of the 1,400 PJ flowing offshore gets redirected home. That’s 280 PJ added to the domestic side. Domestic supply rises from 500 PJ to 780 PJ. Domestic share jumps from 25% to 40%.

That’s a structural shift of where Aussie gas goes.

It won’t happen overnight. Long-term LNG contracts run 15 to 20 years and most were signed years ago. So the share drifts up in lumps as each contract expires and the producer signs a new one with the reservation baked in.

By 2030, you’d expect to see a noticeable shift with the full effect by 2045 or so.

That’s the slow burn. The supply wave is already heading home. It just hasn’t crested.

It’s worth pointing out again that there is still a lot of uncertainty around implementation. Will the natural gas that’s already supplied to the domestic market be counted in the 20% of LNG exports? In its native gas state it’s not LNG. Or is it to be on top?

Either way, there’s a clear intention here to redirect more gas supply to the domestic market.

But there’s more to the story.

The Bigger Move Behind It

While the reservation redirects export gas home over time, four projects are bringing fresh domestic-only supply online. None of them depend on the reservation. All of them stack on top of it.

Bass Strait, Phase 3. Delivers around 40% of east coast domestic gas right now. Woodside takes operatorship from ExxonMobil in 2026. The $228 million Turrum Phase 3 project has Final Investment Decision (FID). Four more potential development wells could add 200 PJ of sales gas across the project life. Bass Strait was set to fall off a cliff. It just got a multi-year extension. Every molecule is domestic. There’s no LNG terminal in Victoria.

Beach Energy (ASX:BPT). ASX-listed pure-play. 100% of east coast production goes domestic. Cooper, Otway, BassGas. Supplies 19% of east coast demand off its own back.

Beetaloo Basin, Northern Territory. Tamboran Resources (ASX:TBN) took FID on the Shenandoah South pilot. First gas Q3 2026. Initial 40 TJ a day, scaling to around 95 TJ a day at Phase 1 expansion. All Phase 1 volumes contracted to the NT Government through 2041. APA Group is studying a US$3 to 4 billion pipeline from the Beetaloo to the east coast with FID targeted 2027. Once that pipeline flows, Beetaloo gas reaches Sydney and Melbourne in the early 2030s.

Narrabri, NSW. Santos’s coal seam gas project. 100% committed to the NSW domestic market. Full ramp at 200 TJ a day for a 25-year field life. Roughly 70 PJ a year. Final approvals still pending but the trajectory is forward.

Add it up. By 2030 to 2032, those four sources could be delivering an additional 150 to 200 PJ a year of domestic-only gas, on top of the existing 500 PJ.

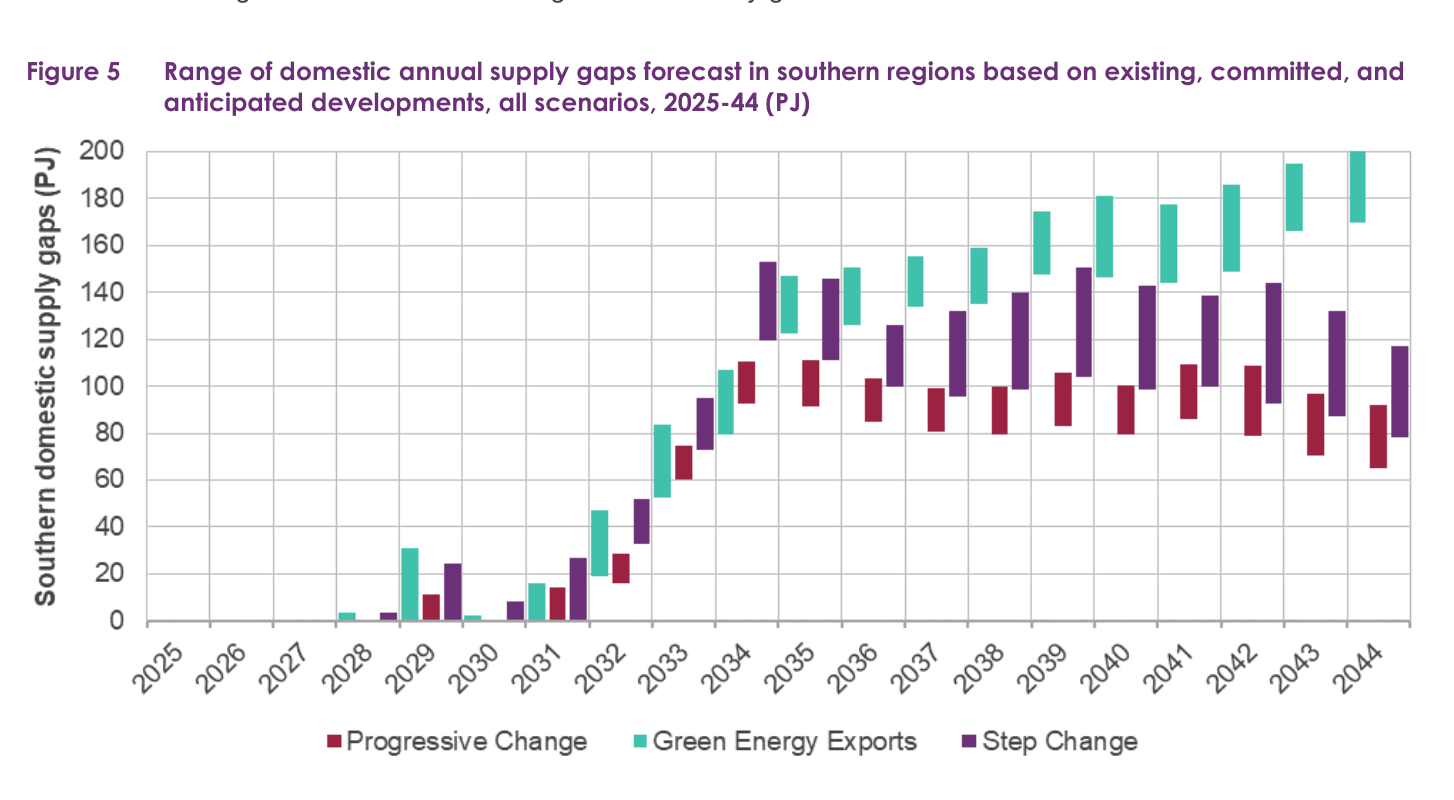

AEMO’s baseline scenario, with only committed projects, runs into a structural shortfall from 2028. The gaps grow into the mid-2030s.

Domestic supply gaps forecast in southern regions (Source: AEMO)

There is however, a path to supply-demand balance, even without the reservation. It requires a lot of moving parts to fall into place.

Pipeline upgrades from Queensland. Southern supply solutions. An LNG regasification terminal as backup. Layer the new supply options on top. The gap could close by the early 2030s and stay closed.

Demand grows over the same window. Coal retirement adds gas peaker load. Yallourn closes mid-2028. Eraring’s extension only delays its end-date. Loy Yang A is underwritten only to 2035. Daily peak gas-fired generation demand is forecast to triple by 2050.

But demand grows from a base of around 500 PJ today to maybe 650 PJ by 2035. Supply can grow faster. The market can move from tight today, to balanced by 2030, to surplus by 2035. This is, however, the optimistic scenario.

Step one, not the end of the move

Once a government has the mechanism, they use it. WA’s gas reservation started at 15% in 2006 under Premier Carpenter. Two decades later the Perth debate is about whether to lift it to 20%. If nothing else, this budget has shown that Labor is willing to do the unpopular things. Like implement the policies that lost them the 2019 election.

The federal version starts at 20%. The draft legislation drops in June with final consultation through July. The first review will land within five years. By 2032 or 2035 the rate could lift to 25% or 30%. New project approvals could carry contingent conditions. ‘Approval granted subject to 35% domestic reservation.’ That’s how every WA project from Gorgon onward got conditioned.

Three things make the ratchet a near-certainty.

Coal is leaving the grid. Renewables need firming. Manufacturers need cheaper energy than overseas competitors pay. The Government has decided gas users matter more than gas exporters. That decision will get reinforced over time, not relaxed.

What today looks like a 25-to-40% domestic re-rate over twenty years could become a 50%-plus domestic re-rate if the rate gets lifted, the approvals get tightened, and the new projects come on as planned.

That’s the supply wave hiding inside the budget.

So, who picks up the cheque?

The Stocks to Watch

Three ways to play the wave. Two ways to watch out for it.

The Three Industrials Riding the Wave

Cheaper, more reliable gas reads through to one place. Industrial input costs.

Orica (ASX:ORI). World’s largest commercial explosives maker. Ammonium nitrate plants run on gas as feedstock. Their Kooragang Island plant alone is one of the largest single gas users on the east coast. When the wholesale price moves, every renegotiation moves with it.

BlueScope Steel (ASX:BSL). Port Kembla is one of the most gas-intensive industrial sites in the country. Reducing agents, blast heat, rolling mill firing. The new electric arc pivot decouples them only in part. For the next decade, cheaper domestic gas reads straight through to BlueScope’s cost base.

Soul Pattinson (ASX:SOL). Now houses the merged Brickworks operation after last year’s $14 billion scheme of arrangement. Bricks need kilns. Kilns need heat. SOL is also one of the cleanest holding-company exposures to Aussie industrial gas users on the ASX, sitting on top of a diversified portfolio of utility-style cash flows.

Three companies. Three industrial users hostage to one input cost. One supply wave that bends the curve their way for the next two decades.

The Two Losers

Santos (ASX:STO) and Origin Energy (ASX:ORG). Both are partners in Gladstone LNG ventures whose new export contracts now carry the 20% reservation. The grandfathering protects existing long-dated offtake agreements, so the near-term hit is small. But the long-term math is brutal. Every new contract sells 20% of its volume into the domestic market at a domestic price by design, while only 80% reaches the seaborne LNG benchmark. New export projects sit on top of a structural ceiling. The market took 3% out of Santos and 1.2% out of Origin the afternoon the policy leaked. The full re-rating still hasn’t shown up.

Woodside (ASX:WDS) ducks the worst of it. Its projects are on the west coast, outside the federal scheme. WA’s older 15% reservation has been Woodside’s reality for two decades. This of course, assumes the policy is east coast focussed, and that the west coast mechanism will remain untouched. That’s a big assumption.

The Wildcard

The cleanest beneficiary of this entire structure isn’t a manufacturer and it isn’t a producer.

APA Group (ASX:APA) owns roughly 15,000 kilometres of gas transmission pipeline on the east coast. Volume-based tariff income. Every gigajoule that flows from Queensland to Sydney is a tariff. Every gigajoule that gets liquefied at Curtis Island and put on a ship is a tariff APA doesn’t collect. The reservation redirects molecules from one of those flows to the other. APA captures the flip.

They didn’t wait. APA is in Stage 3 of its East Coast Gas Grid Expansion. Adds 30% pipeline capacity, completing winter 2028. Stage 3A alone adds 20% more capacity for northern gas going into Victoria. Combined with Stages 1 and 2 already done, APA will have lifted east coast pipeline capacity by more than 50% in five years. They built the pipes ahead of the policy.

APA also lobbied on the record. Their own phrasing.

‘We need to ensure the Federal Government closes this out quickly and delivers an effective domestic gas reservation for the east coast. This provides certainty for customers, consumers and the wider energy industry and ensures reliable and affordable domestic gas remains available to power our economy.’

Add the Beetaloo. If APA takes FID on the US$3 to 4 billion Beetaloo-to-East Coast pipeline in 2027, you’re looking at a second leg of transmission growth running through the 2030s. Tamboran’s wells in the NT, every gigajoule paying APA tariff on its way to Sydney and Melbourne.

APA is the system.

The Edge

Three things to watch over the next twelve months.

One. The draft legislation drops in June. Read the carve-outs, the trigger thresholds, the definitions of ‘export contract’ and ‘new project.’ WA’s reservation has been watered down through fifteen years of negotiated exemptions. The federal one will get tested the same way. The version that passes in October may not be the version the Treasurer announced.

Two. APA’s August result. APA reports FY26 in August. Watch for guidance uplift from the budget changes and a Beetaloo pipeline FID timeline. A lifted guidance for later years like FY28-FY30 will indicate that APA has the scenarios well mapped and they want investors to share in their enthusiasm.

Three. Manufacturer earnings season. BlueScope reports August. Soul Patts in October. Orica in November. Listen for any line in their commentary that flags Aussie gas as a tailwind on input costs, or a domestic capex decision that depends on cheaper energy. When the manufacturers start spending in Australia rather than offshore, you’ll know the impact is big.

Until next time, happy investing.

Izaac Ronay

Sign up to the Explosive Growth portfolio, and follow Izaac Ronay and The Markets IQ on LinkedIn.

Izaac is a broker and trader with Vitti Capital. He brings over 10 years of trading experience with top-tier global trading houses and 20 years of experience analysing and investing in ASX listed equities.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.