Five High-Yield ASX Dividend Stocks: From The Dog House To The Penthouse

This article is for general information only and is not personal financial advice.

The tax rules just shifted under your feet.

Selling for a gain now costs you more. Holding for income costs you less. We made that case last month, when the budget scrapped the CGT discount.

So you went hunting for yield.

Good.

Here are five for your shortlist. They share one job. They pay you to wait.

Their charts share nothing. One sits 44% below its high. One prints fresh records. The rest are scattered in between.

Now flip them over and read the income. The order nearly reverses. The names the market dumped are paying you the most to be patient.

Patience.

We will climb from the rubble to the record. Start at the bottom.

Source: TheMarketsIQ.com, ASX announcements

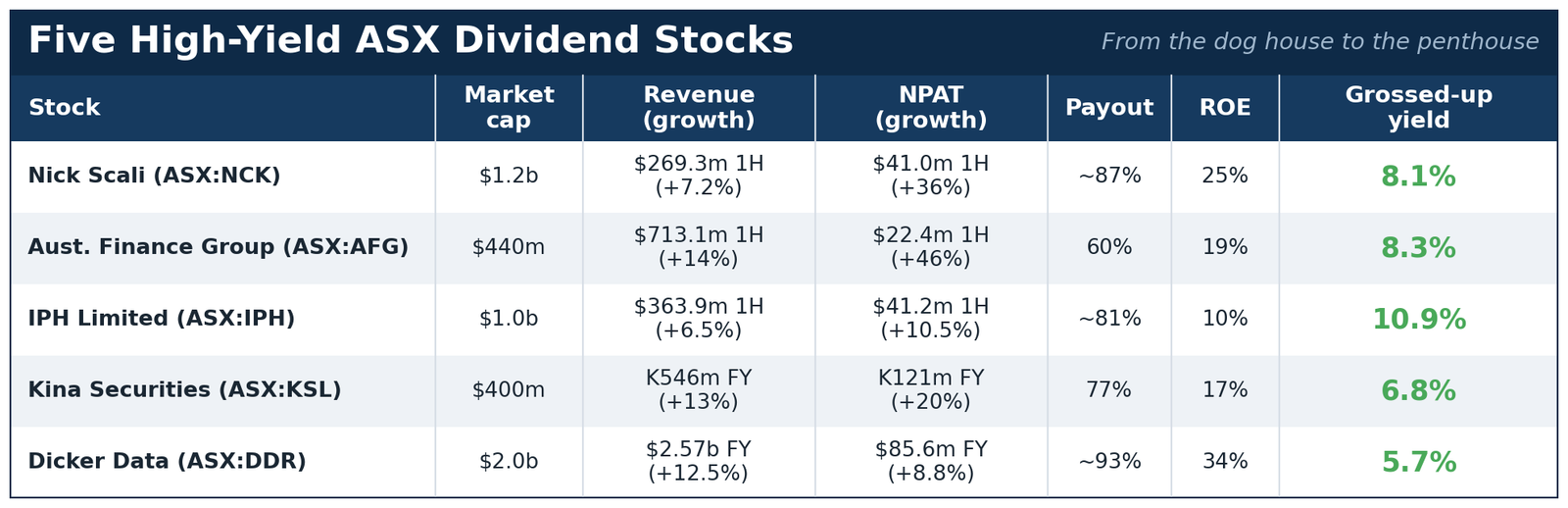

Nick Scali (ASX:NCK), The Sofa Stock Left On The Kerb

Nick Scali (ASX:NCK) sells lounges.

The market is pricing it like it sells typewriters. The stock trades 43% below its peak.

The bull case. These people can buy a rival and digest it.

They proved it with Plush in 2021. They turned the deal into profit, not a hangover.

Now they run the same playbook in Britain. The Fabb turnaround plus a fresh Nick Scali rollout hands you a second engine. That market opportunity dwarfs home.

The numbers still work. A 65% gross margin. A 25% return on equity. Half-year sales of $269m, with earnings up 36%, all funding a fully franked payout.

8.1% grossed-up.

The bear case. Furniture is the first thing shoppers skip when money is tight. High rates sit on it like a heavy guest on a thin couch.

The stock is no bargain at 18 times earnings. It pays out almost 90% of full-year profit, a slim buffer if Britain bleeds before it pays.

Watch two things. The British store economics. The Australian order book.

They flag the turnaround before the dividend does.

The next name has tested its owners for two years. It also runs the nation’s mortgage plumbing.

Australian Finance Group (ASX:AFG) Owns The Mortgage Toll Booth

Australian Finance Group (ASX:AFG) sits in the pipes of home lending.

One in nine Australian mortgages runs through its brokers. Yet the stock sits 44% below its high.

The bull case. FY26 could be its best year ever.

It already booked a record first half. AFG clips a percentage of every loan its brokers settle.

So its income is the average loan size times the number of deals. We mapped that lodgement engine when we asked whether CBA had run too hot.

Two things drive it, and both point up. House prices sit at all-time highs, which lifts the average loan. Property deals are thawing, which lifts the count.

Multiply the two. That is total deal flow. AFG takes its slice off the top.

It showed up in the half. Settlements hit almost $38bn, up 19%. Revenue rose 14%, and earnings jumped 46%. When profit grows three times faster than the top line, that is operating leverage doing the work, fixed costs already covered while each extra loan drops to the bottom line.

The fully franked dividend still eats just 60% of profit. That sits at the floor of its 60 to 80% payout policy, so the payout can climb even if earnings only hold.

8.3% grossed-up.

The bear case. Aggregator margins are thin, near 3%. So volume is everything. And volume bends with rates.

The balance sheet also carries a big securitised loan book. It makes the gearing look worse than it is.

Watch the monthly settlement figures. Watch the next move from the Reserve Bank.

A property rebound makes the year. A rate scare breaks it.

The next name pays more again. It comes from a business the market decided AI would bury.

IPH Limited (ASX:IPH), The Patent Annuity AI Cannot Crack Yet

IPH Limited (ASX:IPH) files and renews patents and trademarks.

It does this across Asia, Canada and Australia. Each renewal is a toll. It falls due every year, through an agent, in every country a firm wants cover.

That is a 62% gross margin annuity in a dull grey suit.

The bull case. The AI scare knocked the stock 27%. The timing is back to front.

Over the next few years IPH should gain more than it loses. It can put AI to work inside its own walls today. Cheaper search, faster drafting, leaner admin. That can widen margins even if revenue only holds.

No client trusts a machine to guard a million-dollar patent. Not until that machine is proven beyond doubt. That proof is years away.

The cash backs it up. Underlying profit was $62.6m for the half. The statutory line, dragged down by paper amortisation, showed just $41.2m. And the board is buying back stock at the beaten price.

That is what people do when they think the crowd is wrong.

10.9% grossed-up.

The bear case. Growth has gone quiet. Group revenue rose just 6.5%, and a Canadian deal did much of that. The organic part was thinner.

The roll-up model leans on debt to fund deals. Debt costs more now. The franking is light at 20%.

The AI threat is delayed. It has not gone away.

Watch the organic growth line. Watch the full-year result in August.

Prove the margin is lifting, and the re-rate writes itself.

Now we leave the dog house. We step into the names the market already loves.

Kina Securities (ASX:KSL) Is Banking A Nation Skipping The Branch

Kina Securities (ASX:KSL) is the headline grabber.

It is a leading bank in an underbanked market. It trades near its highs on an 8% yield. The story is bigger than the number.

The bull case. Papua New Guinea is one of the least banked places on earth.

Its people are leapfrogging the branch entirely. Much of the developing world skipped the landline and went straight to the mobile phone. PNG is doing the same with banking, going straight to the app.

Kina is the disruptor riding that wave. Digital channels now bring in about half its revenue, while the old guard sleeps.

The growth backs the story. A 17% return on equity. A 22% net margin. Profit up 20%, and a dividend up 25% in local kina.

When a market is built from scratch, you back the builder.

6.8% net.

The bear case. The passport is the risk.

There are no franking credits. The profit is earned offshore. And PNG skims 15% off the dividend at the border (baked into our net yield above). An Australian holder rarely gets it back.

The kina keeps sliding. That is why 25% dividend growth at home shrank to 8% by the time it reached Sydney.

The stock is thin, near $266,000 a day.

Watch the kina. Watch the digital customer count. Watch the bad-debt ratio.

The disruption is genuine. The currency is the toll you pay to own it.

The last name is the one everybody wants. That is exactly why it pays the least.

Dicker Data (ASX:DDR), Nvidia And Microsoft’s Hired Muscle

Dicker Data (ASX:DDR) sells the picks and shovels of the tech boom.

It moves the hardware and licences every upgrade runs on. It sits a whisker below its all-time high. The others nurse their bruises.

The bull case. This one has two edges.

Two.

It is one of Nvidia’s authorised Australian distributors, plugged into the chip the whole AI build-out is fighting over. It also rides the Windows 10 cut-off. Corporate Australia must refresh its machines now, like it or not.

Add a 34% return on equity. Add revenue up 13%. Add a fully franked dividend. A loved business on a genuine tailwind.

5.7% grossed-up.

The bear case. Popularity has a price. You pay it at 22 times earnings, the richest tag here.

Distribution is a thin game, near 3% net. The payout already sits at the top of its 80 to 100% range, so the next rise has to come from profit, not a fuller slice. The stock is funded by debt, so higher rates lift the cost of holding it.

Watch the AI server orders. Watch the working capital.

The chips, the refresh, the franking all point up. But the share price has already heard the good news.

Five stocks. One chart that runs from rubble to record. An income league that runs the other way.

The market lavished its attention on Kina and Dicker Data. It handed its fattest grossed-up income to the names it had written off.

Until next time, happy investing.

Izaac Ronay

Sign up to the Explosive Growth portfolio, and follow Izaac Ronay and The Markets IQ on LinkedIn.

Izaac is a broker and trader with Vitti Capital. He brings over 10 years of trading experience with top-tier global trading houses and 20 years of experience analysing and investing in ASX listed equities.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.