- March 3, 2026

Don’t Overlook ASX Biotech

This article is for general information only and is not personal financial advice.

In the computer game Fallout 2, the main mission is to save your tribe from drought. Along the way, you’re offered side quests — optional detours that help you level up, gather gear, and pass the time.

Quests like retrieving a stolen watch from a radioactive scorpion, becoming a boxing champion or getting an old car running again.

A side quest is how Australian investors seem to view biotech.

Highly optional and maybe an interesting way to waste your time (and money).

We’re addicted to our boom-time mining profits and the too-big-to-fail safety of our highly protected banking sector.

And we’re maybe just suspicious of anyone wearing a lab coat.

ASX investors didn’t blink before lending extreme valuations to uranium stocks. We don’t need to understand the economics (or lack thereof). If we can dig it up and sell it, it’s time to buy.

Just like the lithium boom and inevitable bust that came before, there are plenty of punters willing to throw down money on uranium stocks, with very little understanding of the sector.

Yet when it comes to a cure for cancer, a treatment that slows the progression of Alzheimer’s, or a blood test that detects viral and bacterial infections, we’re strangely reluctant.

Blind greed is enough to back a lithium miner, the same way we would bet on a horse. For biotechs? It’s suddenly too much risk, or when will I get a dividend?

But our collective blind spot for biotech is a great opportunity if you’re willing to spend the time to understand the sector. It’s a lot of work, but the payoffs can be exceptional. And it doesn’t have to be ‘all in’ on 13 black.

Right now, two of the best names in the sector have been beaten up. One is a global powerhouse in the middle of a messy self-inflicted restructure. The other is a radiopharma rocket that had one flat quarter and got treated like it had a terminal illness.

Both are worth attention.

The Two Games of Biotech

Before we get into names, here’s a simple framework for thinking about biotechs.

Game One: Industrial Biotech. These companies have:

- Products

- Customers

- Revenue

You model these roughly like you’d model any high-quality business — with a bit more tolerance for pipeline potential.

Think CSL (ASX:CSL) and ResMed (ASX:RMD). Price to Earnings is as good a metric as any, and a discounted cashflow analysis is actually appropriate and not just tossed around for an analyst to sound smart.

Game Two: Small-Cap Catalyst Biotech. It’s all theoretical until the catalyst hits. Trial readouts, FDA decisions, reimbursement approvals — these are the fundamentals. The calendar is your research tool, not the income statement.

Cash position gets dwarfed by a single regulatory approval. Very few of the companies in this basket are profitable. The revenue showing up on their PnL is most likely a government R&D rebate.

Most retail investors get annihilated in Game Two because they can’t get their head around it.

I can’t count the times I’ve excitedly discussed LDX and their bacterial vs viral blood test, or the cortisol mechanism in Alzheimer’s that ACW is targeting or Recce’s new anti-infective implications, just to be asked if they pay a dividend.

My heart always sinks at that question. With it, I know I’m likely talking to someone with a narrow way of looking at companies.

Now — the big names.

CSL, The Fortress That Keeps Shooting Itself in the Foot

CSL (ASX:CSL) is supposed to be bulletproof.

A genuinely rare thing. An Australian company that became a global leader not by digging something out of the ground, but by building IP, infrastructure, and a collection network that competitors would need decades and billions to replicate.

The plasma franchise alone — CSL Behring — is a structural oligopoly. It has a highly defensible position.

So why has the stock been hammered?

Part of it is genuinely out of management’s hands. US influenza vaccination rates have fallen sharply, and CSL’s Seqirus vaccine arm is directly exposed. US Health Secretary Robert F. Kennedy Jr. has been openly sceptical of vaccine programs. That’s a headwind no CEO can charm away.

But here’s what investors need to say out loud: CSL has also been making unforced errors, and the market is right to punish them.

We’re seeing more fumbles than a Manly Sea Eagles NRL game.

The Vifor acquisition — the iron and nephrology business CSL bought for around US$11.7 billion in 2022 — has been a persistent drag. Generic competition has hit iron products, the strategic rationale has been questioned repeatedly, and it added a layer of complexity to a company that was already managing two large divisions.

Then came the Seqirus demerger saga.

CSL told investors to expect a June 2026 demerger. Then walked it back, saying they’d wait for US market conditions to improve. The decision might be defensible.

The whiplash is not.

Markets hate being surprised. They especially hate the feeling that management is reacting to events rather than controlling them.

And then, in August 2025, CSL announced a major restructuring, closing 22 plasma centres, cutting staff, booking large charges. Restructuring isn’t inherently bad — but a restructuring that large is usually the receipt you get after years of slow drift. You don’t close 22 centres because everything was running beautifully.

The punchline came in February 2026 with a sudden CEO change. Paul McKenzie was out, Gordon Naylor stepped in as interim, and a global search for a permanent leader began. The board’s message was clear, performance has been unacceptable.

So what’s the investment case?

The market is pricing CSL like the moat is eroding.

The better-calibrated read is that CSL has an execution problem, a credibility problem, and a hostile external environment. But, the underlying plasma franchise is still one of the best businesses on the ASX.

If new management can simplify the portfolio, rebuild communication discipline, and stop stepping on rakes, the stock rerate from here is significant.

If they can’t, you own a slower version of a good business at a permanently lower multiple.

That’s the bet. Eyes open.

Telix, the Growth Story that Keeps Getting Interrupted

Telix Pharmaceuticals (ASX:TLX) has been collecting bad news for a while now.

The FDA knockback on their therapeutic pipeline was real, it was painful, and the market treated it accordingly.

Before that, there were pipeline delays, capital questions, and the usual biotech turbulence that shakes out anyone who wasn’t paying attention to the underlying business.

Then Q4 2025 came in roughly flat against Q3 — around US$208 million versus US$206 million. The market panicked again.

The FDA knockback was the loudest. But a resubmission is in progress, and the science hasn’t changed. What the market priced as a structural failure was, in retrospect, a delay.

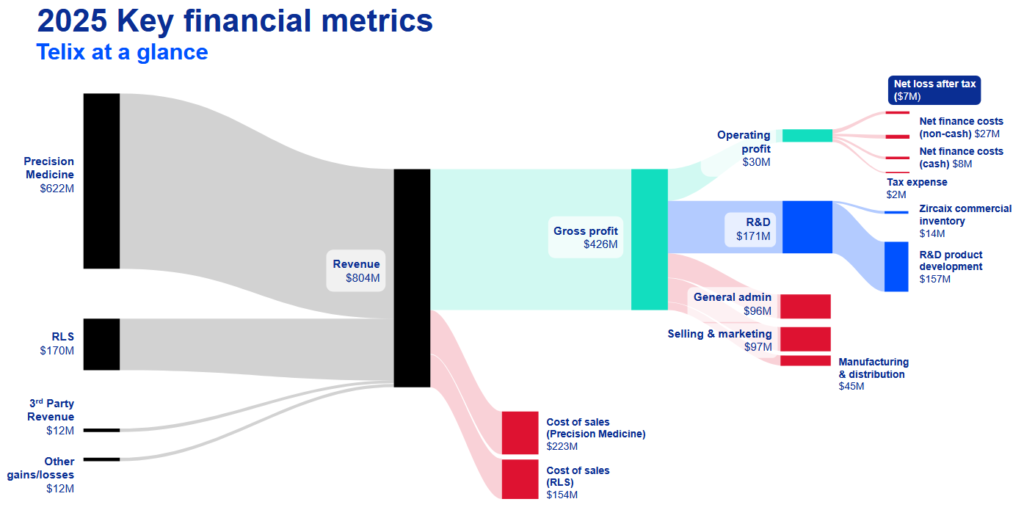

Zoom out for a moment. Telix reported FY2025 revenue of US$803.8 million, up 56% on the prior year. They guided FY2026 at US$950–970 million. This is a business generating serious money, growing seriously fast.

One quarter ticking sideways inside that trajectory is not a structural problem. It’s a data point. Seasonality happens. Ordering cycles happen. Constraints happen. A company doesn’t become a different company because one quarter looked boring.

The more interesting question — the one that barely got asked amid the hand-wringing — is whether Telix is building a platform or riding one product. Because those two things have very different answers to a flat quarter.

The evidence points firmly toward platform. The core prostate imaging product, Illuccix, is established and scaling.

Gozellix extended the US footprint. But the infrastructure story is where it gets genuinely interesting. Radiopharmaceuticals aren’t like pills — isotopes decay, you can’t warehouse them and wait for orders, the logistics network is inseparable from the product itself. Telix grasped this early.

The RLS Radiopharmacies acquisition brought 31 licensed radiopharmacies across major US metro areas, giving them last-mile delivery alongside manufacturing capability. In this sector, that’s a structural moat being built in real time.

They spent US$157 million on R&D in FY2025 and guided US$200–240 million for FY2026. They could turn off the R&D faucet tomorrow and show instant profitability. Instead they’re laying groundwork for decades of future profitability, and building a strategic advantage over rivals.

So add it up: an FDA knockback that’s moving toward resubmission, a flat quarter in a business growing at 56% annually, and a platform investment thesis that hasn’t shifted at all. The pattern here isn’t decline.

It’s a growth story that keeps getting interrupted, keeps getting written off, and keeps continuing anyway.

Delayed growth and dead growth look identical in a panicked forum thread.

They don’t look identical in a pipeline, a manufacturing network, or a revenue trajectory. The distinction is worth holding onto.

Clarity, the Rising Threat Worth Watching

If Telix is the established commercial engine, Clarity Pharmaceuticals (ASX:CU6) is the clinical-stage challenger in the same radiopharmaceutical space.

Clarity is building theranostic products — the diagnostic-plus-therapeutic model where you use radioactivity both to image and to treat cancer. It’s earlier stage, which means the risk profile is different.

More catalyst-dependent, more binary, more upside if it works.

Here’s the thought experiment worth running: what would a Telix-Clarity combination actually look like?

You’d be merging Telix’s distribution muscle, commercial revenue, and US infrastructure with Clarity’s next-generation pipeline assets. Bigger platform. Broader portfolio. More negotiating power with hospitals and insurers. The kind of scale that makes a company genuinely hard to compete against.

There’s no deal. No announcement. This is speculative.

But it’s a useful exercise because it forces you to think about what actually creates durable winners in radiopharma.

Scale plus logistics plus pipeline. That combination is the moat.

Small-Cap Biotech: Stop Modelling, Start Calendaring

For the smaller end of the sector, here’s the most important mental shift you can make.

Stop trying to value these companies like linear-growth businesses. Start tracking their catalysts like events.

The catalyst IS the fundamental. A Phase 3 readout, an FDA decision, a reimbursement approval, an interim data analysis — these are the moments that either change the probability landscape entirely or reset it to zero. Until one of these lands, the stock price is mostly noise.

A few current examples worth tracking:

Lumos Diagnostics (ASX:LDX) is chasing a CLIA waiver for FebriDx, its respiratory illness test. Right now it’s stuck in moderate-complexity lab settings. A CLIA waiver opens the entire point-of-care market — pharmacies, GP clinics, urgent care. That’s the catalyst. That’s the whole story until it resolves.

Actinogen (ASX:ACW) had an interim analysis from its XanaMIA Alzheimer’s trial in late January 2026. The independent data monitoring committee recommended continuing without amendment — which is biotech-speak for ‘the safety data looked fine and the trial isn’t obviously failing.’ Not the explosive green light, but importantly, still showing enough promise to continue on.

Orthocell (ASX: OCC) is the quiet ramp that doesn’t get enough attention. Seven consecutive quarters of record revenue, with the most recent hitting $3.2 million for the December 2025 quarter.

Small numbers in absolute terms, but the trajectory is consistent and the US rollout is an ongoing catalyst.

Recce Pharmaceuticals (ASX:RCE) has a registrational Phase 3 trial running in Indonesia for R327 topical gel in diabetic foot infections.

Phase 3 data and regulatory submission are targeted around early 2026, with potential commercial launch in the first half of the year. If that data lands well, the story flips from clinical to commercial.

But the implications go well beyond this first indication. The company is setting itself up to tackle a pipeline of conditions.

Imugene (ASX:IMU) acquired an allogeneic CAR-T candidate — azer-cel — from Precision BioSciences and has been building toward a pivotal trial in 2026.

The ‘allogeneic’ part means off-the-shelf. Instead of harvesting and engineering each patient’s own cells (slow, expensive, limited scale).

If the clinical signal holds and manufacturing is credible, the M&A potential here is substantial. Big pharma pays up for scalable oncology platforms.

The Edge

The ASX underprices biotech. It always has. The sector is lumped in with mining logic, or written off because people remember the graveyard of small-cap science projects that never made it past a PowerPoint.

That trauma creates a recurring blind spot.

CSL isn’t a broken business.

It’s a world-class franchise being run poorly, wearing hostile external headwinds, going through the painful process of getting itself back in order.

If management stabilises and regains credibility, the rerate is meaningful. If they can’t, you own a slower version of a great business.

Telix is not stalling.

It had a flat quarter. The platform — commercial revenue, owned distribution infrastructure, deep R&D — is exactly what a dominant radiopharma company looks like at this stage of development.

As for small-caps, get to know the catalysts and the timeframes. Stay on top of the binary events that can change the probability curve.

The investors who get hurt in biotech are the ones who buy after the catalyst has already fired and the stock has already doubled. The ones who do well know what’s coming and position before it lands.

Don’t fear the sector. Learn the rules of the game you’re actually playing.

If you want The Markets IQ take on great biotech businesses with big catalysts on the horizon, check out the Explosive Growth research page.

Until next time, happy investing.

Izaac Ronay

Sign-up to the Explosive Growth portfolio, and follow Izaac Ronay and The Markets IQ on LinkedIn.

Izaac is a broker and trader with Vitti Capital. He brings over 10 years of trading experience with top-tier global trading houses and 20 years of experience analysing and investing in ASX listed equities.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.