Boring to Brilliant: ASX's Automotive Winner From Trump’s Tariff Tantrum

Trump is Back Baby!

Not to toot our own horn, but TheMarketsIQ called his return just before the election here. That's right. We were the only ones.

OK. Enough hyperbole.

The result wasn't entirely surprising. As we mentioned, "...the best indication of a Trump victory is the betting odds. Polymarket has Trump with a 57.6% chance of victory."

If you want to see what people value, watch how they spend their money. And what better use case than election betting. The polls indicated a closely contested election.

Fake poll! Sad!

We found out in 2016 how wrong the polls are. The only surprise here is that we are still talking about them as if they mean something.

Well the Trump return has thrown the markets into a spin. We're all scrambling to position for the best winners and trying to drop the losers as elegantly as possible. No small feat, given the big change agenda we're facing.

Of all the winners and losers, we've got an established and profitable ASX player that could be one of the biggest beneficiaries. We'll talk about how that could play out, but before we get to that, let's set the scene.

What Trump Round 2 Means for the Markets!

One of Trump's core promises was to go toe to toe with China again. It's all about bringing jobs back to land of guns and fast food.

What better foe than Communism? And what better example of functional "Communism" than China.

President Xi is possibly the greatest Capitalist of all time.

And he's A communist!

If that's not a threat to Trump's masculinity then I don't know what is.

Trump is hyper-competitive. It's not a secret. He want's to be number one, and he wants the USA to be number one.

Well attaining number one status is one thing, but keeping it is another. Right now China is throwing punches at the USA. They are taking jobs, technology, trade secrets...punch after punch after punch.

Trump's style is to punch back twice as hard

We've all seen it.

With his political opponents his reprisals might stop at sharp words. But with other countries he gets heavy handed. He's no stranger to the use of Tariffs. In 2028 he brought in a range of tariffs against a range of friend and "foe" countries, with China a primary target then as well.

A lot has changes since then, and one of the biggest developments has been the rise of EVs.

Traditional automakers have found themselves on the back-foot against a slew of young ambitous electric vehicle manufacturers, with a good swathe of them hailing from China.

The automobile is one of America's great symbols. Ford is arguably the most important automaker ever, and to see the industry in decline in the US is an affront to Trump's sensitive nature.

So, it's no wonder that's one of his primary targets in his second term. This is his last chance to make his mark on US history as a president, and he's not going to pass up how good this opportunity is. He's got more power than last time, with the House, the Senate and the popular vote all backing him up.

He's aiming for a whopping 60% tariff on Chinese-made cars entering the U.S. It's a bold move that's sending shock-waves through the auto world. That's going to make the US market a dead end for Chinese automakers.

Chinese automakers have been working hard to crack the U.S. market. Companies like BYD and NIO were banking on American consumers as a major growth engine. But with Trump's tariffs on the horizon, that door is slamming shut.

Not only that, but the secondary - and unintended - consequences could be massive.

Chinese car-makers are scrambling to find new markets for their electric vehicles. The goal is rich developed markets with weak or no domestic car manufacturers.

The EU is a tough sell, given the abundant local industry, strong brand loyalty, existing tariffs and over the top regulatory environment.

Canada is certainly one of the prize markets, although there will certainly be competition from other North American made cars.

Australia could be the perfect opportunity. Sure, we're a smaller population with a large geographic sprawl.Why Australia?

On the plus side, we let our auto industry drown a long time ago, and brand loyalty with it. We're a rich country and despite that a lot of us are sleeping in cars now due to a lack of housing supply. That makes the humble car a much more important possession.

But there's more to the story.

Aussies are starting to get curious about this whole EV thing. We're starting to overcome this idea of them ruining our weekend. A lot of us have been in one now, or have a friend or family member with one.

The general feeling is that they're quite practical. After all, how often are we actually doing that 1000km trip in one day?

Plus, we're not a one car household country anymore. On average there are 1.8 cars to every household in the lucky country these days.

It's not such a big deal to have one car that is recharged off the solar panels at home, given there's also a 4WD diesel ute in just about every driveway it seems.

The big challenge for EVs down under is serving the low cost but still decent quality market segment. That's where the Chinese automakers are well placed to step in. BYD, for instance, is the world’s largest EV manufacturer, and they’ve got the production power to flood the market with well-priced options.

The opportunity here is immense, and savvy investors will want to pay close attention as this story unfolds.

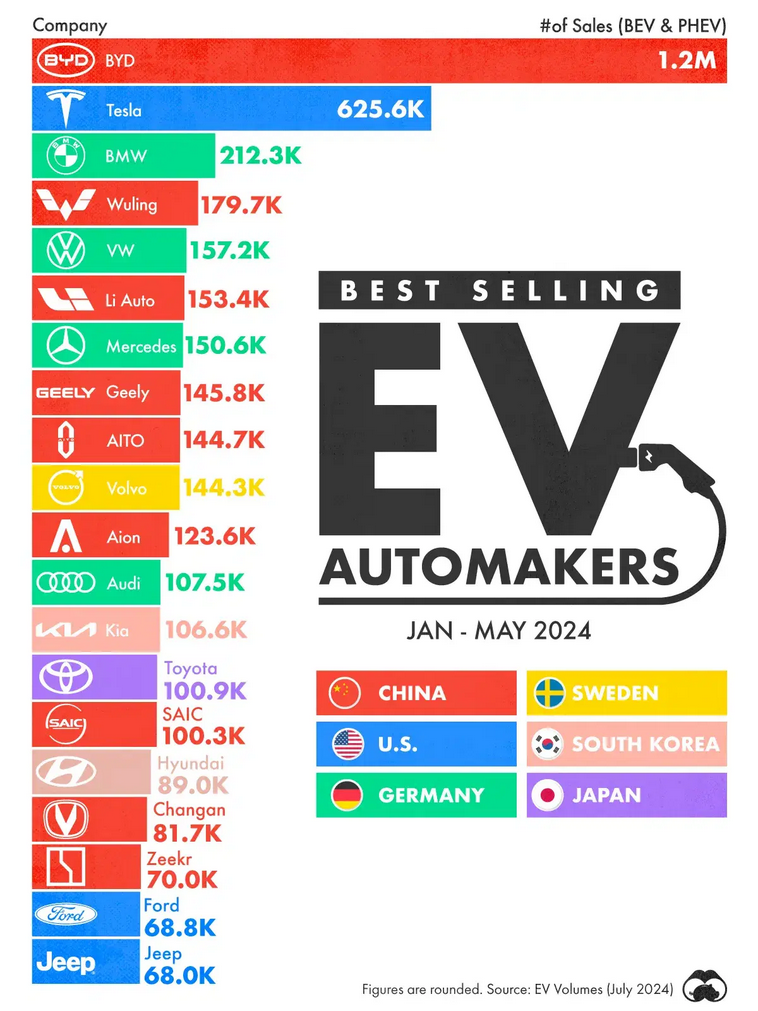

The Market Leader and the Gatekeeper

BYD is now the biggest supplier of electric vehicles to the world, if we include both Battery Electric Vehicles (BEV) and

Source: EV Boosters

In China, they've got about a third of the EV market, and 20% of all new auto sales. It's easy to see where the success comes from. BYD cars are practical, reasonable quality and - most importantly - affordable. The bottom of the range Dolphin hatch comes in under $37,000 at the time of writing.

It's not the cheapest car to be found, but it presents good value, especially as EVs are still fetching a pretty premium over ICE vehicles.

So, with their value focused offering, BYD is well placed to tackle the middle of the market in Australia.

Now here's something you might not know. Every BYD sold into Australia goes through a company called EV Direct. It has exclusive rights to sell BYD down under.

The company uses a direct to consumer model, similar to Tesla. By cutting out the dealers, costs are dramatically reduced.

But it does partner strongly with an ASX listed company called Eagers Automotive (ASX:APE). And with good reason. APE is the biggest shareholder of EV Direct, holding 80%.

It helps with the distribution and servicing of vehicles that EV Direct brings in. So, APE get's 80% of what EV Direct is making as the distributor, and they get fees from assisting EV Direct with distribution and servicing.

It's a sweat deal given the opportunity for BYD in the Australian market place.

APE may well be the company best placed to capitalise on this opportunity.

But it doesn't even stop at BYD. APE has the biggest dealership network in Australia. This makes them an ideal first partner for other Chinese automakers looking to establish a foothold in Australia. Brands like NIO, Xpeng, and others might find in Eagers the perfect local partner, leveraging their existing infrastructure and market connections.

APE is perfectly positioned to be the key gateway for these Chinese EVs to reach eager Australian buyers.

Eagers Automotive is already one of the largest automotive retail groups in Australia, with a solid footprint in both urban and regional areas. This extensive network allows them to effectively serve the entire country, ensuring that as more EV models are introduced, they have the capability to bring them to a wide audience.

Company Snapshot

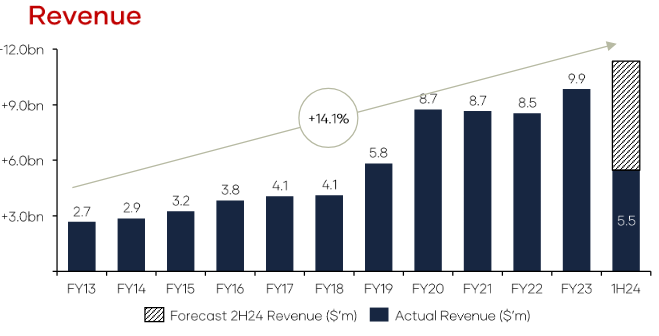

Eagers Automotive has had a great start to 2024. The first half revenue increased 13.4% over 2023 to $5.5 billion. The Underlying Operating EBITDA was up 4.6%. It was a record half year EBITDA result, which showed the benefits of recent acquisitions and spot on execution.

A dividend of 24 cents was paid for the half year.

For the full year, the company is forecasting a record revenue result. The past decade has been steady growth, as showing in the following chart.

Source: Eagers Automotive

The new vehicle order books remains strong, despite clearing most of the Covid backlog. There's also $297.4 million in cash at the bank. Syndicated is up substantially to $325.3 million.

The business is not without it's pressures however, and floor finance is one of the trickier aspects of car dealerships. Floor stock is generally secured with debt, which comes at a hefty price tag.

As interest rates move around, this can make the bottom line performance of car dealers very cyclical.

APE has seen Underlying EBITDA margin contract from 5.3% to 4.9%. Underlying PBT was a 12% fall as well to $182.5 million.

Normalising inventory levels means more selling opportunities, however it also means higher cost of debt. Inventory increased from $1,620 million to $1,837.4. This equates to 42 days of unsold supply and 22 days of sold but not delivered.

These are key metrics for APE, which they need to keep as low as possible, so as to maximise return on each vehicle sold.

It's important to note that the majority of the impact on these metrics comes from growth initiatives in both greenfield sites and acquisitions. Like for like measures are much more stable.

There's still plenty of borrowing headroom for APE, and current debt levels are certainly not excessive. We expect these growth initiatives could pay off in a big way over the next five years, particularly as the EV Direct partnership continues to gain traction.

Final Thoughts

Trump's tariffs are creating a unique disruption to the automotive industry. As Chinese EV makers look beyond the U.S., Australia is emerging as a priority market. Eagers is perfectly positioned as the gateway to make that happen.

It’s exclusive partnership with BYD, along with their capacity to potentially partner with other Chinese automakers, gives them a distinct strategic advantage. They are not just riding the wave of growing EV adoption in Australia, they're leading it.

For investors, this is a compelling opportunity to ponder. Eagers Automotive could see significant growth in sales and market share as more Chinese EV brands enter Australia. The company is poised to be a major beneficiary of the redirection of Chinese EV exports, and this positioning could translate into substantial upside for its stock price as the market develops.

Investors should watch closely for announcements of new partnerships, increased BYD sales, and potential expansion into supporting additional Chinese brands—all of which could serve as catalysts for Eagers Automotive's stock to ape higher over the coming years.

This is just one example for you to consider of how Trump's change agenda could have far reaching impacts. Positioning before these policies come into effect could make a massive difference to your 2025 portfolio returns.

Source: TradingView

- ASX:APE

- Automotive

- Leadership

- BYD

- Tesla

- TSLA

- Trump

- Tarrifs

- Eagers Automotive

- EV Direct

- Financials