Lumos Diagnostics Update

The Major Catalyst is Imminent

General advice only – prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

The decision window is here.

We first introduced Lumos Diagnostics (ASX:LDX) as a classic asymmetric healthcare setup. A proven test. A massive clinical need. One regulatory gate standing in the way of scale. Since then, the story has matured.

The PHASE Scientific agreement locked in distribution and guaranteed revenue. It was a game-changer, and the market paid attention.

Our thesis hinged on LDX clearing the CLIA. That’s when we expect the real payoff.

And we are getting close.

The decision is expected by the end of March 2026.

The Lumos Diagnostics investment case

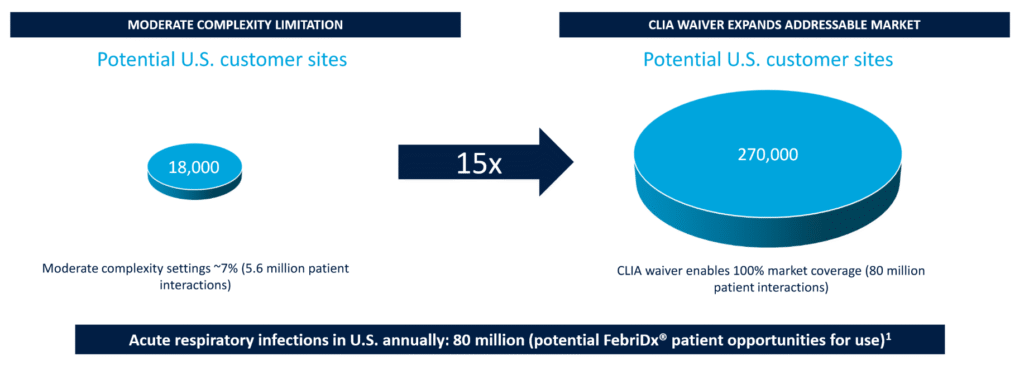

FebriDx is a 10-minute finger-prick test that differentiates between bacterial and viral respiratory infections. That distinction drives antibiotic prescribing behaviour. Antibiotic misuse is a global problem.

If doctors can quickly rule out bacterial infection, they prescribe fewer antibiotics. That improves outcomes and reduces cost. The product already works. It’s cleared for moderate complexity settings.

The missing piece is CLIA waiver approval, which allows use in low complexity settings such as primary care clinics and urgent care.

That would put LDX ahead of the competing bacterial vs viral infection tests that are already in the market. None of them have the CLIA waiver. MeMed BV is the closest, with FDA approval and talk of a CLIA waiver variant.

The CLIA waiver would give LDX a first mover advantage into use cases without directly competing products. In other words, a game-changer.

It also unlocks the full value of the PHASE Scientific deal.

The PHASE deal is gold for Lumos investors

Before PHASE Scientific, investors had to underwrite two risks. Regulatory approval and commercial adoption.

After PHASE, adoption risk largely disappeared in the US.

The six-year exclusive US agreement carries a minimum contracted value of US$317 million if the CLIA waiver is granted, based on agreed minimum order quantities.

Converted at roughly 0.66 AUD/USD, that represents about $480 million over six years as the contractual floor. That’s $80 million per year on average as a minimum.

If the waiver is not granted, the agreement guarantees ~$38 million (US$25 million) over six years. That converts to roughly $6 million per year.

Those numbers are the minimum under the contract.

Minimum.

Say it with me.

M I N I M U M.

No distributor signs up to guaranteed minimum order quantities unless they believe demand comfortably exceeds that number.

If anything, counterparties want to lock in a floor that sits below what they believe is achievable. It would be reckless to commit to buying more stock than you can sell.

Which means the US$317 million headline shouldn’t be viewed as a cap.

It’s a base case under approval.

The CLIA waiver signal

The application was filed in August 2025.

Clinical trial data showed 99.1% concordance on bacterial positives and 98.4% concordance on non-bacterial samples. Performance in untrained hands was the critical metric.

That’s an important consideration for the FDA. If the test is taken out of the laboratory and put in the hands of the average doctor, nurse or pharmacist, are they going to be able to use it correctly?

Well, the data suggests yes. Which shouldn’t be a surprise, since we’re all pretty well trained in lateral flow cassette tests from all those Covid tests we had to take.

They’re very similar. I think we can all manage.

Since filing, the case for a positive decision looks stronger. As per the company’s recent presentation:

‘Lumos received feedback from the FDA at the 90-day time frame from submission. FDA asked a number of questions, for minor changes to instructions and for a small usability assessment. All now completed and responses submitted to FDA in late January.‘

The company’s communication with shareholders and its preparation for manufacturing readiness signal a very high level of confidence.

That’s not a guarantee, of course, but it is a positive sign.

We still frame approval probability at above 80% and consider this a conservative estimate.

The CLIA approval scenario

Assume CLIA is granted.

Revenue under the PHASE agreement averages $80 million per year.

Lumos has previously reported gross margins in the low 60% range. Diagnostics manufacturing at scale can support margins in the 60-80% range depending on volume and mix. Let us use a conservative 65% gross margin.

On $80 million revenue, that equates to $52 million gross profit annually.

Operating costs will rise with scale. Sales support, quality, regulatory oversight, administration. But much of the heavy R&D burden is already absorbed.

Assume $25 million annual operating expenses at scale.

That leaves roughly $27 million EBITDA.

After tax, net profit could reasonably sit around $20 million per year once steady state is reached.

At today’s market cap of $230 million, that is roughly 11.5x earnings.

For a contracted, high-margin healthcare diagnostics company with growth expectations, that’s cheap.

On a revenue basis, you are paying just under 3 times annual revenue.

Again, not demanding.

And remember, that is based on minimum contracted volumes.

If demand exceeds those minimums and revenue trends towards $100 million plus annually, the numbers shift quickly. $30 million net profit on a 15 times multiple implies $450 million valuation. That is roughly 56 cents per share.

Of course, this is all assuming they get the green light.

The downside scenario

If CLIA is not granted, revenue under PHASE defaults to roughly $6 million per year minimum over six years.

Minimum. Possibly my new favourite word.

It does not mean that PHASE suddenly loses interest in selling the test. It means they are no longer contractually obligated to the higher volumes.

The test doesn’t become worthless.

The clinical need does not disappear.

Moderate complexity settings remain accessible.

International markets remain available.

Importantly, PHASE would not have negotiated minimum order quantities at US$25 million over six years unless they believed meaningful demand exists, as we’ve already covered.

So in a no-waiver world, $6 million per year is the contractual base. It’s not the ceiling. PHASE could still pursue higher volumes if demand supports it. Lumos could also pursue additional partnerships in other geographies or segments.

Growth would be slower. Scale would be smaller. But the business would still have value and still carry a growth narrative.

Let’s dig deeper.

Assume $10 million revenue annually in a no-waiver world. That is above the minimum but conservative relative to potential moderate complexity sales and international growth.

At 60% gross margin, that is $6 million gross profit.

Assume tight cost control keeps operating expenses near $12 million.

Losses would narrow significantly compared to historical burn, and management could pivot to right size the business.

In that world, the market would likely still value Lumos as a growth stage diagnostics company with proven technology but slower US penetration.

Early stage diagnostics companies with credible growth trajectories have historically traded anywhere between 2 to 5 times revenue, where there is high uncertainty.

When there’s a high confidence of strong growth, those numbers can stretch to 10x.

If the CLIA waiver isn’t granted, the market will likely become overly pessimistic about LDX’s short-term growth.

At $10 million in revenue, even a 4x multiple implies a $40 million valuation.

But it could also easily stabilise in the $60 million to $100 million range after the initial shakeout. It might take 2-3 months to find the next comfortable price level.

That implies material downside from $230 million, but not collapse to zero.

The damage will depend on how well LDX can deliver growth with approved use cases, other deals they can land and any new product announcements.

Expected value

Let us model it cleanly.

Success valuation. Assume $20 million steady state earnings. Apply a 15 times multiple. That is $300 million equity value.

Downside valuation. Assume $80 million equity value as a midpoint of slower growth but an intact platform.

At 80% probability of success.

0.8 times $300 million equals $240 million. 0.2 times $80 million equals $16 million.

Combined expected value equals $256 million.

Current market cap is roughly $230 million. Still slightly under the expected value.

And that does not factor in upside beyond minimum order quantities.

Recommendation

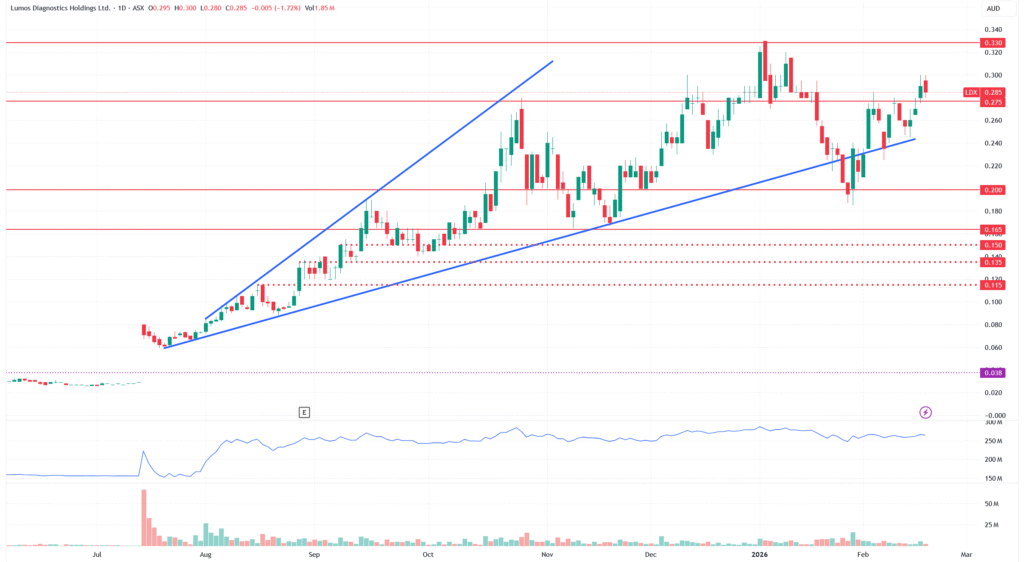

The asymmetry has narrowed since our original entry near 13 cents.

But it hasn’t disappeared. We are no longer paying microcap lottery pricing.

We are paying for a high-probability regulatory outcome, with contracted revenue in place.

The market already assumes success is likely.

We agree.

The question now is magnitude.

If approval lands on time, attention will shift from probability to scale. Investors will start modelling revenue ramp, margin expansion and earnings power.

If approval is delayed but not rejected, volatility will rise. That may create an opportunity.

If approval is rejected, the stock will fall hard. But the business remains real, and the growth case does not vanish completely.

At 28.5 cents and $230 million market cap, Lumos sits on the edge of a decision that defines the next five years.

The window is open.

Now we wait.

We maintain our BUY recommendation for Lumos Diagnostics (ASX:LDX) and raise our buy-up-to price to 30 cents. There’s still asymmetric upside at current prices. We expect to see a big move on the CLIA waiver decision announcement, and caution investors to think about risk when sizing their positions.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital may hold positions in companies mentioned or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.

The analyst(s) responsible for preparing this research note certify that the views expressed in this report accurately reflect their personal views about the companies mentioned and their securities. No part of their compensation is, or will be, directly or indirectly related to the specific recommendations or views expressed herein. The analyst(s) and/or their associates may hold an interest in the companies mentioned.