Flip a Coin on Alzheimer’s

A near-term binary catalyst with asymmetric upside

General advice only – prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

Actinogen Medical (ASX:ACW) is setting up as one of the most binary biotech plays on the ASX.

Timing is everything.

The company is running a late-stage Alzheimer’s trial called XanaMIA. The interim analysis is due in late January 2026.

As in, any day now.

If XanaMIA survives that interim read, the market will have to re-rate the stock. If it fails, it will be ugly.

There’s no gentle middle ground.

Actinogen’s whole pitch is brain cortisol. They are targeting the enzyme 11β-HSD1 to reduce cortisol inside the brain without shutting down cortisol production system wide. The drug is Xanamem, also called emestedastat.

It’s oral, once daily, and designed to reach key brain regions like the hippocampus and frontal cortex.

The current wave of Alzheimer’s drugs is dominated by antibodies. They can work, but they come with real baggage, infusion logistics, monitoring, and serious side effects in some patients. A safe oral therapy that meaningfully slows decline would be a very big deal.

That’s the dream.

Now the reality.

XanaMIA is a phase 2b/3, double blind, placebo controlled trial. Treatment is 36 weeks. It targets mild to moderate Alzheimer’s patients who are biomarker positive using elevated pTau181 in blood. The primary endpoint is a scoring system called the Clinical Dementia Rating-Sum of Boxes (CDR-SB), which regulators recognise.

The trial is being run in Australia and the US. Recruitment is now closed. Interim analysis is the immediate catalyst, with final topline results in November 2026.

So, this is not a tiny early stage punt. This is the closest thing biotech gets to a proper binary catalyst.

Assets

1) The Alzheimer’s program, XanaMIA and XanaMIA-OLE

XanaMIA is the core asset. It is where nearly all the value sits.

Actinogen has tried to stack the deck in its favour in a few ways.

First, the biomarker filter. They’re using baseline blood pTau181 to enrich the trial for true Alzheimer’s pathology.

This matters because Alzheimer’s trials are infamous for burning years and cash due to poor patient selection. Clinical diagnosis alone is noisy, and a meaningful fraction of patients in historical trials never had Alzheimer’s biology in the first place.

By requiring pTau181 positivity at baseline, they can be far more confident they are recruiting patients with genuine Alzheimer’s disease rather than lookalike conditions that have been misdiagnosed. That materially improves statistical power and the chance of detecting a real drug effect.

Second, dose selection is dialled in.

The company is running 10 mg once daily. They point to multiple independent trials, a PET imaging study showing high target engagement even at 5 mg daily, and a safety database of around 400 participants across eight studies.

Dose selection is a balancing act between safety and efficacy, and Actinogen enters this trial with strong prior human data, giving them a solid chance at getting it right.

Third, they are building the regulatory story while the trial runs. In September 2025, Actinogen received a Type C meeting written response from the FDA on the Alzheimer’s program. They reached a common understanding on the pathway to marketing approval and the required manufacturing, clinical, and nonclinical activities.

This tells potential partners the FDA has at least looked at the plan and the company knows what is coming.

There’s also an open label extension, XanaMIA-OLE planned for up to 25 months. All participants get active drug. It’s meant to evaluate safety and a limited set of efficacy endpoints. It’s planned to commence in Q1 2026.

The interim analysis is the near term gate. Actinogen has been clear about what it is. The independent Data Monitoring Committee (DMC) will review unblinded data for safety and efficacy futility. This is not a big marketing event with fancy charts.

If it’s clearly not slowing disease progression, or if it’s just too dangerous, the trial is stopped.

A positive interim result doesn’t necessarily mean the whole trial will be a success. But it should provide us with a lot of information to make a prediction.

In November 2025, the company reported the first DMC meeting outcome. The DMC reviewed safety data for 153 participants and recommended the trial continue without amendment. No efficacy was evaluated at that meeting.

That doesn’t mean it works. It means the safety profile is still behaving.

In December 2025, recruitment was closed and the 246th participant had been randomised and commenced treatment. That locks the data set. Now the clock runs toward trial completion.

2) Depression program, XanaCIDD

The depression angle is not the main game right now. But it’s not fluff.

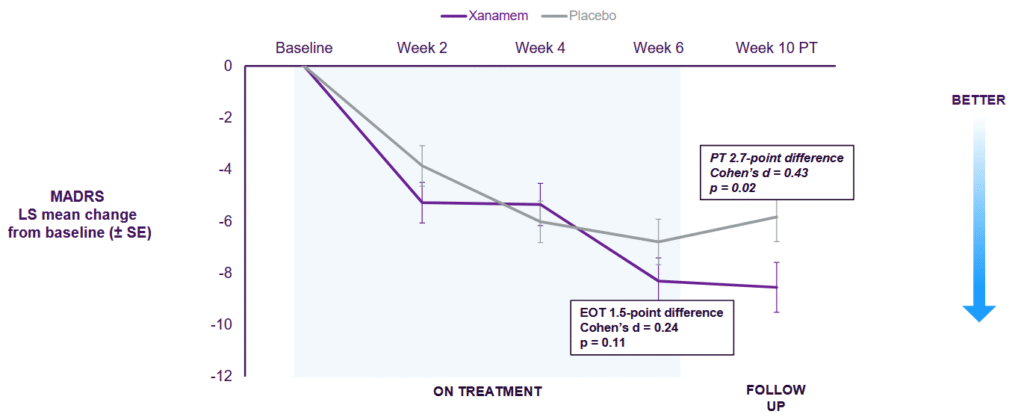

Actinogen ran a phase 2a trial in 167 patients with moderate, treatment resistant depression and baseline cognitive impairment.

It was double blind, placebo controlled, six weeks, with 10 mg Xanamem once daily. Results were reported in August 2024.

The company reported clinically and statistically significant benefits on depression symptoms using MADRS and PGI-S. Cognition improved in both groups. It was an unexpected curveball when the placebo group saw a dramatic improvement as well.

While the strong placebo showing has stalled progress on the depression indication, it doesn’t mean it’s dead in the water. There is potential for a more robust trial design down the track, which may show a benefit above placebo.

The result also validates the cortisol mechanism in humans. If you want to believe the Alzheimer’s story, you want as many human signals as possible.

There’s also regulatory work on Major Depressive Disorder (MDD).

The FY2025 reporting noted a Type C meeting on MDD with the FDA in March 2025 and a common understanding on additional trials and studies required for marketing approval in that indication. That’s longer dated and almost certainly partner dependent. Still, it keeps the platform story alive.

3) Manufacturing and commercial readiness

Biotech dies in the small details. Formulation, manufacturing scale, supply chain and regulators. It’s all about getting to market quickly, reliably and on budget.

Actinogen has locked in a commercial tablet formulation. They’ve flagged Catalent as the US manufacturing partner.

It sounds boring.

It’s not. This is the stuff partners want to see before they take you seriously. Having manufacturing squared away is also critical for regulatory approval. The FDA wants to make sure a drug maker isn’t going to just make some ‘innocent’ tweaks to the product after it has received the rubber stamp.

In Alzheimer’s, manufacturing readiness is often the hidden bottleneck that delays partnerships even when clinical data is strong.

Why brain cortisol is a decent bet

Most Alzheimer’s trials fail for reasons that are hard to forecast from the outside. Wrong target. Wrong stage of disease. Wrong endpoint. Wrong patient selection etc.

Actinogen is taking a swing at a pathway that has two nice qualities.

One, it is mechanistically plausible. Cortisol is the body’s stress hormone. Chronic high cortisol is associated with hippocampal damage and cognitive decline, and higher cortisol has been linked to hippocampal atrophy and progression risk in Alzheimer’s cohorts.

Actinogen is not trying to abolish cortisol. They are trying to reduce cortisol regeneration inside the brain by inhibiting 11β-HSD1.

Two, it is not a copy paste of the amyloid antibody trade. The market already knows how to price amyloid antibodies. Big pharma can fund them. Doctors can prescribe them. And patients still face meaningful monitoring and Amyloid-Related Imaging Abnormalities (ARIA) risk, including MRI monitoring requirements that can tighten as safety learnings evolve.

If Xanamem works, it is a different category. Oral. Once daily. Potentially easier to scale. Potentially easier to combine with other therapies. It becomes a companion piece to the Alzheimer’s toolbox, not a competitor fighting for the same infusion chair.

This is important to keep in mind. Xanamem doesn’t have to show itself to be the best standalone defence against the disease for it to be a success. If it’s safe and has a benefit, it may end up being part of a stack of compounds used to treat Alzheimer’s.

Management and execution

This is a scientific execution story, not a marketing story.

CEO and MD is Dr Steven Gourlay.

He’s been leading the company through clinical development and investor engagement. He’s also sunk $2 million of his own cash into the company to become a large shareholder.

That’s solid belief. Exactly what you want to see from the guy running the whole operation.

The company has also appointed a Chief Commercial Officer during FY2025 as part of its commercial readiness push.

In biotech, commercial is part of the trial. Manufacturing, formulation, labelling, regulatory pathway, payer conversations, partner conversations. All of it starts early or you lose time.

The other execution tell is the cadence of milestones. Recruitment has closed and the DMC has already cleared safety once.

Financials

This is where the story gets a little uncomfortable.

At 30 September 2025, Actinogen reported cash and cash equivalents of $10.4 million. They also reported pro forma cash of $12.4 million after the receipt of the FY2025 RDTI refund.

In the same Appendix 4C, they disclosed net operating cash outflow of $6.1 million and an estimated 1.71 quarters of funding. That estimate is mechanical, not gospel, but it tells you the obvious.

The trial costs money.

Current cash will see the company through to mid 2026.

If the interim analysis is positive, the financing options get much better. If it’s negative, financing becomes a survival exercise.

So you have to frame ACW as what it is. A catalyst led biotech. Not a steady compounder…yet

The good news is that the company has access to the Australian R&D Tax Incentive. That is meaningful non dilutive support.

We expect a decisive move to lock further funding after the interim readout. That could be in the form of a cash up front commercial deal, or more likely they’ll tap the market for further cash.

So expect a capital raise announcement in the next few months.

However, if the interim read is juicy, we expect that next raise will be conducted at a higher valuation.

Valuation Context

The current market cap is about $160 million.

Using the last reported pro forma cash of $12.4 million from the September 2025 quarterly, you get a rough enterprise value around $147 million. That’s not a precise number because cash will have moved since then. But it’s the right ballpark for the debate.

So what are you paying for?

You are paying for a shot at an Alzheimer’s drug that can clear interim futility and then go on to read out in late 2026. You are also paying for a strong bet on a depression program that has already shown signal (sort of).

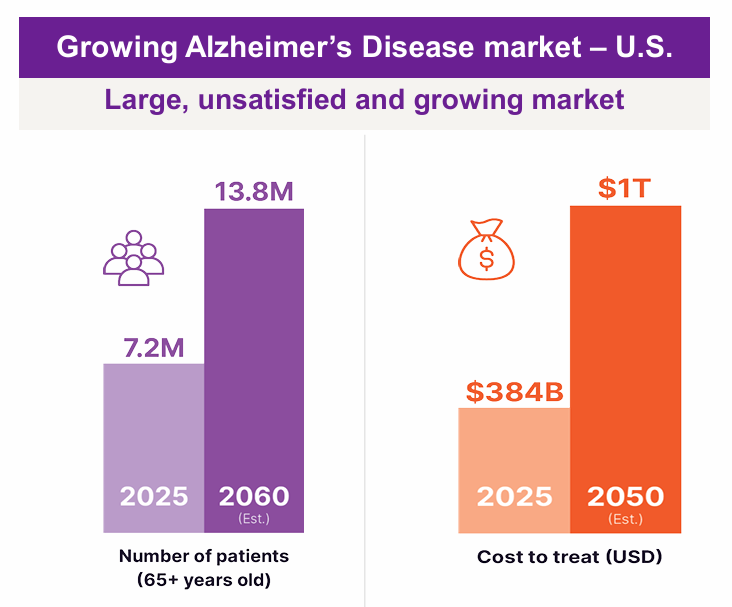

Is $147 million enterprise value cheap. If you think there is a real chance of a positive Alzheimer’s outcome, yes. Because Alzheimer’s is a monster market.

It’s also massive in pure numbers. In the US, an estimated 7.2 million people aged 65 and older are living with Alzheimer’s in 2025. Even small efficacy can be a big commercial prize. And an oral drug is attractive.

Is it expensive?

If you think the trial fails at interim, yes. Because the market will instantly re-price this toward bottom-drawer scraps.

The market is being forced to pick a side very soon.

We’re betting that this is an asymmetrical opportunity, with a high chance of success and potentially big re-rating if it hits.

Outlook and Catalysts

This stock lives and dies on a handful of dates.

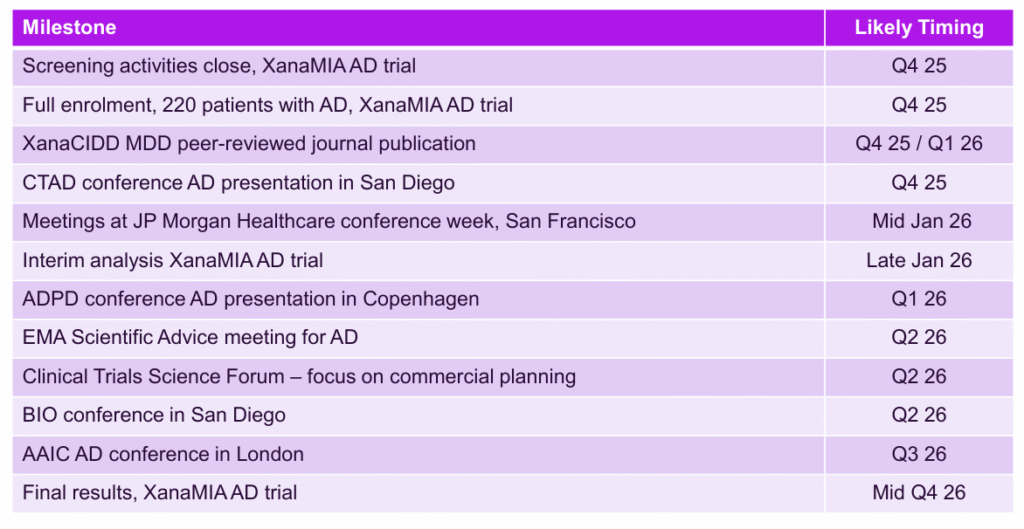

Late January 2026 is the big one. That is the interim analysis result from the independent DMC. If the trial passes futility and safety, you get a de-risked path to final readout. You also get a much easier partnering conversation. And an easier funding conversation.

Q1 2026 matters too. That is when the open label extension is meant to commence. OLE programs can keep patients engaged and can create additional safety and durability data. It’s also just newsflow to keep investors interested.

November 2026 is the other monster. That is final topline results. This is the real value moment if it works.

Between those, the company is trying to do what smart biotechs do. Get in front of the right people. The company is in the midst of a conference tour.

A capital markets and partnering exercise. It’s time to start shopping the goods to see what interest they can get in terms of funding and commercial partnerships.

There are also medium term regulatory catalysts. The company has flagged an EMA Alzheimer’s meeting in 2026 based on the September 2025 FDA written response.

If you want to sell a drug globally, you need those meetings.

Risks

Interim analysis failure.

If the interim futility assessment says stop, the stock gets smoked. A soft landing is out of the question.

Final efficacy failure.

Even if the interim passes, the final endpoint can still miss. Alzheimer’s is graveyard territory for drug developers.

Funding and dilution.

The company will almost certainly move to raise further funding before the final readout. If the market doesn’t find a reason for exuberance in the interim readout, that could mean heavy dilution and/or investors having to open their wallets again.

Mechanism risk.

The cortisol hypothesis is interesting and there is human data support. But Alzheimer’s is complex. Reducing brain cortisol may not be enough.

Competitive landscape.

Anti amyloid antibodies are gaining traction and new mechanisms are coming. If a wave of safer and more effective therapies arrives, commercial opportunity can shift.

Recommendation

Actinogen is for investors who understand biotech risk and who want exposure to a near term binary catalyst.

The interim analysis is the whole reason to look at this stock right now. The timeline is tight. The company has closed recruitment. The first DMC safety review was positive and did not require amendments. Regulatory planning has been de-risked with the FDA Type C written response.

At a roughly $160 million market cap, you are not paying a ridiculous premium for this shot. You are paying for the possibility that Xanamem becomes a viable, safe oral therapy in a market that is starving for better options.

But position sizing matters. This is a high volatility name. Treat it like a biotech option. If you cannot handle a 50% drawdown in a day, do not pretend you can.

We recommend a BUY on Actinogen Medical (ASX:ACW) with a Buy-Up-To price of 7 cents. We stress the importance of proper position sizing to account for the highly binary nature of this stock this year.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital may hold positions in Actinogen Medical (ASX:ACW) or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.

The analyst(s) responsible for preparing this research note certify that the views expressed in this report accurately reflect their personal views about Actinogen Medical (ASX:ACW) and its securities. No part of their compensation is, or will be, directly or indirectly related to the specific recommendations or views expressed herein. The analyst(s) and/or their associates may hold an interest in Actinogen Medical (ASX:ACW).