Audeara Update

Hearing tech nanocap sees strong growth

General advice only – prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

Audeara (ASX:AUA) has hit the holy grail of high-growth ASX small-caps. Operating cash-flow positive.

…Just.

We’re talking $356 thousand.

We’re being a little bit cheeky here, since they did it on the back of a $1.22 million Research and Development tax refund.

But, it’s still a sign that the company is heading in the right direction. Operating leverage is high, and revenue is growing rapidly. Add in a dash of time, and you’ve got a recipe for positive and growing cash-flow and profit.

We’ll discuss the financials and the looming catalysts a bit further on.

If you haven’t read our initial write-up on AUA, we suggest you check it out first. It covers the business in more detail, as well as our thesis for the stock.

You can check it out here.

So, let’s jump into the recent developments and how they’ve changed our thesis.

Japan is now in play through a distribution agreement with Eyear System Inc. The deal requires Eyear to purchase initial minimum order quantities.

China is also gaining traction. The Eastech licensing pathway has progressed to first commercial purchase orders.

More than just revenue, these orders show the deals have substance to them, and business partners are seeing something valuable in AUA’s tech.

Audeara secured NMPA certification for its China hearing aid launch, which is basically the difference between ‘interesting story’ and ‘you can actually sell the thing.’

The business model is starting to widen.

The market still thinks of Audeara as a consumer product company. An upstart small ASX earphones producer taking on the giants in audio-tech.

But the BIG opportunities are in the nooks and crannies that no one is paying attention to.

The company’s hearing algorithm is a winning lottery ticket squished in between the couch cushions.

The white label licensing orders are a fifty dollar note waiting patiently in the pocket of your winter jacket.

The Optek agreement is the clearest example.

Audeara’s AUAI algorithms are being licensed for integration into Optek system-on-chip platforms on a fee-per-chip basis. That’s the kind of embedded distribution that can scale fast if OEM brands get on board.

Of course, it’s all speculative until those orders roll in.

But think about this. If one big brand – like Philips – chooses AUA’s algorithms for one of their headphone models, it could completely change the company’s trajectory.

This is still a micro-cap. Execution risk is still real. But the nature of the risk has changed. Deals are happening. Orders are flowing.

It’s now not so much about ‘can they do it?’

It’s, ‘how quickly can they do it?’

Financials

Q2FY26 Update

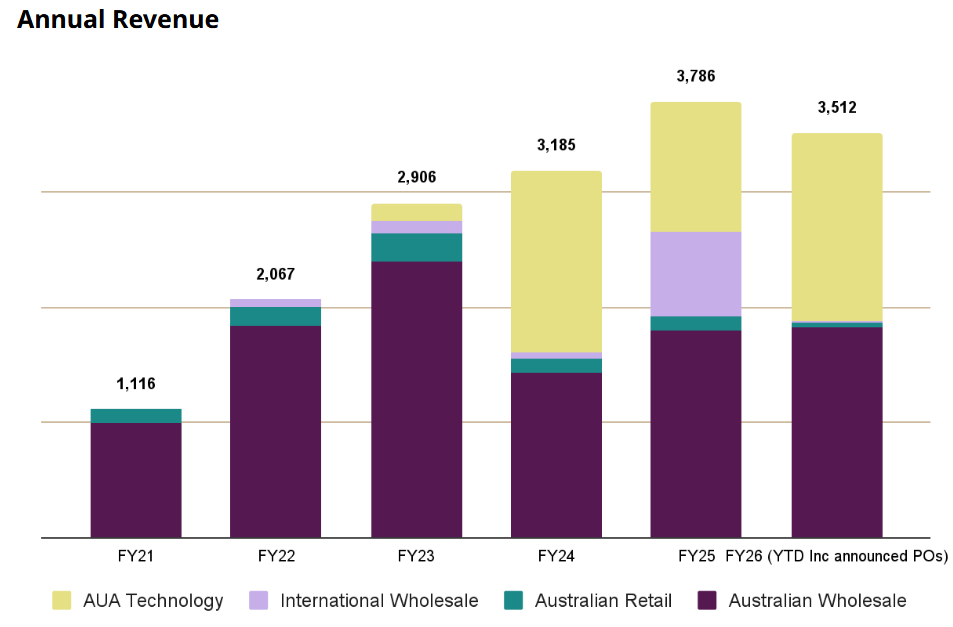

The 2QFY26 quarterly report delivered a solid result. Revenue came in at $1.43 million, a 5.9% fall from Q1, but importantly a 274% increase on 2QFY25.

Combined with a $560 thousand purchase order to be recognised in Q3, it brings FY26 revenue to date to $3.5 million.

This is a fantastic result. While the numbers might not look big, AUA made $3.8 million in revenue for the whole of FY25.

So, we’re seeing very strong growth in these numbers.

The best part is, most of these new deals and offerings have barely started.

For 1HFY26 as a whole, we saw revenue of $2.95 million, a ~64% increase, or $1.15 million on 1HFY25. This excludes the big order to be recognised in 2HFY26.

Operating leverage is kicking in nicely. We previously commented that a $3 million increase in revenue should easily add $1 million to net profit.

Well gross profit increased by 109% or $511 thousand to $980 thousand.

That’s a roughly 44% gross margin on incremental revenue. That suggests $2.3 million in revenue is required for $1 million in gross profit. The total gross margin for the half-year came in at 33.2%, up from 26% in 1HFY25.

Let’s take a look at how that translates to the NPAT level.

AUA is being extremely tight on the cost control front. There were no notable changes to the cost structure.

It’s also worth noting that a substantial uplift in the R&D tax offset, rising by 53% to $572 thousand. There was also an additional government grant of $51 thousand. All up, ‘Other income’ increased by $252 thousand.

The NPAT loss has reduced to just $593 thousand, down 57% from $1.38 million. That’s $787 thousand lower.

That translates to a 68% marginal NPAT margin. Once we remove the change in ‘Other income’, the change is a more modest 33%.

That’s spot on $3 million additional revenue to bring in a further $1 million in NPAT, as we predicted.

While revenue is starting to punch out bigger numbers, it’s important to note that cash receipts lag revenue. For Q2, cash receipts came in low at $732 thousand.

That brings us to the next important point.

Cash is King

In our initiation on Audeara, we identified the cash position as a primary risk for investors.

Not that we think the company will close the doors. But, we anticipate a capital raise this year. But as we pointed out, a few more things going to plan, and it could be at a much higher share price.

At the end of December, cash and cash equivalents sit at $737 thousand, down from $1.21 million in the prior quarter.

The company put $837 thousand net into loan repayments and loan fees.

That $737 thousand is looking rather thin.

Outlook and Catalysts

Audeara has identified four strategic areas of focus for the remainder of FY26.

- Australian wholesale channel consolidation aimed at increasing efficiency.

- Turning AUA Technology discussions into signed deals and tangible orders.

- Supporting the roll-out of hearing aids in China, with the aim of growing market share.

- The international expansion of Auracast sales.

We previously noted that profitability is possible within 12-24 months, and we maintain that view.

Revenue is growing quickly, and margins are expanding as well. Orders are lumpy, so individual quarters may vary.

We reiterate our view that a major US partnership could be transformative. Additionally, at such a low market cap, the company has the potential to become a takeover target in the future.

The biggest ongoing catalysts we foresee are new distribution deals, new orders under these deals and quarterly cash-flow updates.

Path to Profitability

In our last report, we noted:

‘Our base case revenue for FY26 is $6 million, or a ~60% increase on FY25.

The rationale for such a big step up is the multitude of new deals that the company has just started landing.

Still, confidence in the exact number is low. A range between $4.5 million and $8 million is realistic depending on timing of shipments and licensing milestones.

Our forecast is for a bottom line loss of ~$1 million.’

Our forecast remains largely unchanged. However, our confidence has increased. We now see a likely full year revenue result in the $6-7 million range, with surprise potential skewed to the upside, given the large number of deals in negotiation and with orders pending.

Risks

For a more comprehensive overview on how we see the risks, please refer back to our previous write-up.

We will highlight some minor changes to risks, as we see them.

- Cash Flow and Capital Risk

The cash position has decreased to $737 thousand. While we expect cashflow to start catching up to revenue, there’s always a chance that buyers don’t pay their invoices. If this were to happen in particular, it would leave the company in a cash crunch. The most obvious risk from this is a capital raise, which we expect would be well supported. - Partnership and Key Account Risk

The company continues to diversify business models and partners. We see this risk as decreasing as further orders are received from new clients. The reliance on Zildjian alone lessens with each new overseas order that comes in. - Regulatory and Market Access Risk

The NMPA certification in China shows that the company is capable of navigating complex approval structures. This reduces regulatory and market access risk in China, but also gives us confidence in their ability to do the same again in new jurisdictions.

Recommendation

Audeara continues to land deals and tangible orders from new geographies and products. We see the story continuing to derisk over time, with the most notable risk continuing to be a capital raise.

The $12.7 million market cap looks cheap in the context of the very strong revenue growth.

At current levels, the market is valuing Audeara at roughly 2x FY26 revenue. That’s a fraction of comparable high-growth, high-margin businesses. Even a modest 3–4x revenue multiple would imply a much higher share price.

There’s a clear path to profitability, although not guaranteed.

We continue to be impressed by the very high calibre of business partners that Audeara has been able to attract, with the likes of Shokz, Zildjian, and Optek.

We recommend a ‘Buy’ on Audeara (ASX:AUA) at current prices, and raise our buy-up-to price to 10 cents.

Investors should consider the appropriate sizing for their account, given the lower liquidity, small market capitalisation and high chance of a near-term capital raise.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital may hold positions in companies mentioned or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.

The analyst(s) responsible for preparing this research note certify that the views expressed in this report accurately reflect their personal views about the companies mentioned and their securities. No part of their compensation is, or will be, directly or indirectly related to the specific recommendations or views expressed herein. The analyst(s) and/or their associates may hold an interest in the companies mentioned.