ASX Market Outlook: Pre-Open Brief 28.03.2025

ASX Stock Market Outlook

It's looking like a bumpy end to the week.

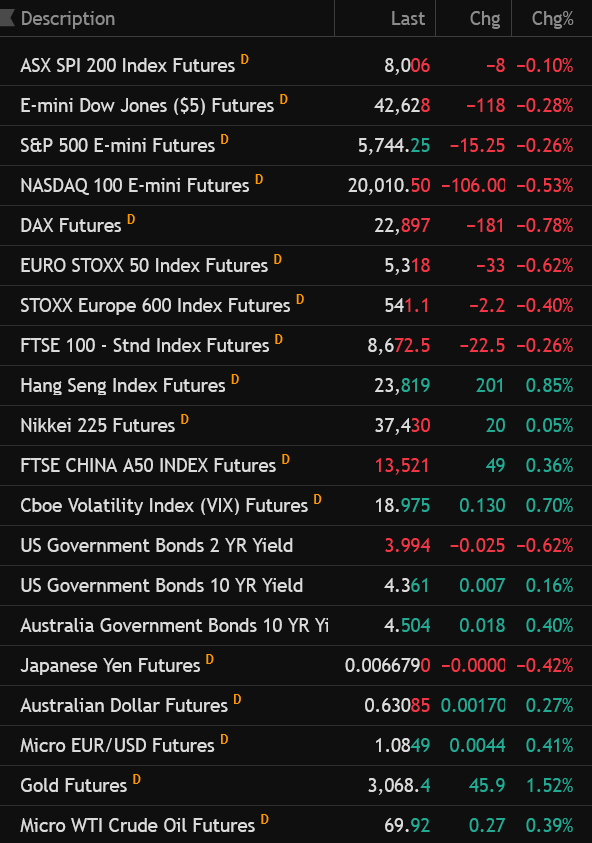

ASX SPI 200 futures are down 0.10% overnight. Wall Street was soft with the S&P 500 E-mini futures down 0.26%, Nasdaq 100 futures dipped 0.53%, and the Dow slipped 0.28%.

The bad news is that the US is markets are currently pointing to a mildly red and very bearish looking doji bar for the week, unless we get some action tonight. That's an ugly look so early in the bounce and would be taken as a sign of big falls to come from many.

In Europe, things looked heavier. DAX futures slumped 0.78%, EURO STOXX 50 dropped 0.62%, and the broader STOXX 600 was off 0.40%. Big money is rotating defensively while the ECB stays hawkish and growth expectations fall off a cliff.

Asia is the only thing keeping the global market from rolling into the weekend in a fetal position. Hang Seng jumped 0.85%, and China A50 added 0.36%, possibly riding renewed stimulus hopes out of Beijing. Even Japan chipped in, sort of, with the Nikkei edging up 0.05%.

Bond markets are quiet, though Aussie 10-years crept up to 4.504%, mirroring a slight uptick in US 10-year yields. The Aussie dollar is stable at 63.08 US cents, and gold just keeps charging — now sitting at US$3,068/oz, up 1.52%.

The Play Today

With tech futures wobbling again and rate-sensitive sectors jittery, investors may try to front-run a long weekend. Gold is your friend and miners could show strength at the open. Energy stocks are in no-man’s land. Crude is sluggish (WTI +0.39%) but not crashing, which means oil majors may just tread water.

Watch for another round of tactical selling in tech and cyclicals. Semis have lost steam globally, and local names like XRO and WTC could feel some of that chill. Lithium and iron ore miners might get some love after rumors about Chinese stimulus have caught some attention.

Beware of intraday reversals and the potential for heavy momentum into the close today.

Major Themes Driving the Financial Markets:

Inflation in Japan: The return of inflation to Japan has major implications. Japanese Government Bonds are tanking as the market factors in higher rates over time. This has the potential to lead to a highly disruptive unravelling of the Yen Carry Trade.

Trade Tensions and Tariffs: The Trump administration's tariff policies continue to inject volatility into global markets. The potential for higher inflation and slower growth—stagflation—remains a concern. Nasdaq futures are up again overnight. AI, semis, and mega-cap tech are leading the charge globally. Can Aussie tech keep up?

Tech Sector Dynamics: Significant movements in major tech stocks, particularly companies like Tesla and Alphabet, highlight the sector's sensitivity to broader economic indicators and policy decisions. Investors should monitor these developments closely.

Economic Data to Watch this Week:

Economic Data to Watch This Week:

Tuesday: Japanese BOJ Meeting Minutes

Wednesday: Australian CPI, UK CPI, US Core Durable Goods Orders

Thursday: US GDP Final,

Friday: US Core PCE

Reading List

MIQ: The Yen Carry Trade Unwind

Global Market Prices

Global Markets(Source: TradingView)

ASX Sector Financials

Watch Financials today for signs of follow through buying. A third green day will get some excitement going.

ASX Financials sector index (Source: TradingView)

ASX Stock to Watch: Australian Finance Group (ASX:AFG)

Australian mortgage aggregator and non bank lender AFG could be one to watch today. It’s benefitting from the strength in financials and the strong housing outlook.

ASX Stocks to Watch (Source: TradingView)

The Daily Brief is prepared in partnership with Vitti Capital.