Lumos Diagnostics (ASX:LDX) Update

A Clear Growth Runway

General advice only — prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

In February we covered how the CLIA waiver was the catalyst for Lumos Diagnostics (ASX:LDX), and that it was close. You can read that note here: Lumos Diagnostics Update – The Major Catalyst is Imminent.

On 27 March the US FDA handed FebriDx its 510(k) clearance with a CLIA waiver. That clearance gifted Lumos a 15x jump in its addressable market, from a lab-bound niche to more than US$1 billion.

Then the stock fell by more than half.

Ouch.

The big binary decision came back with a tick of approval. The science stacks up. The reimbursement pays. And the share price has slid from 28.5c when we last wrote to 11.5c today.

The risk now is whether the company can sell enough tests, fast enough, before the cash runs thin. We’ll dive into what’s changed, what you’re getting at 11.5c and what to watch out for.

Push, Pull, Prove

The CLIA waiver grants access to use cases where FebriDx has no direct competition. Their nearest direct competitor is MeMed BV, with no CLIA waiver.

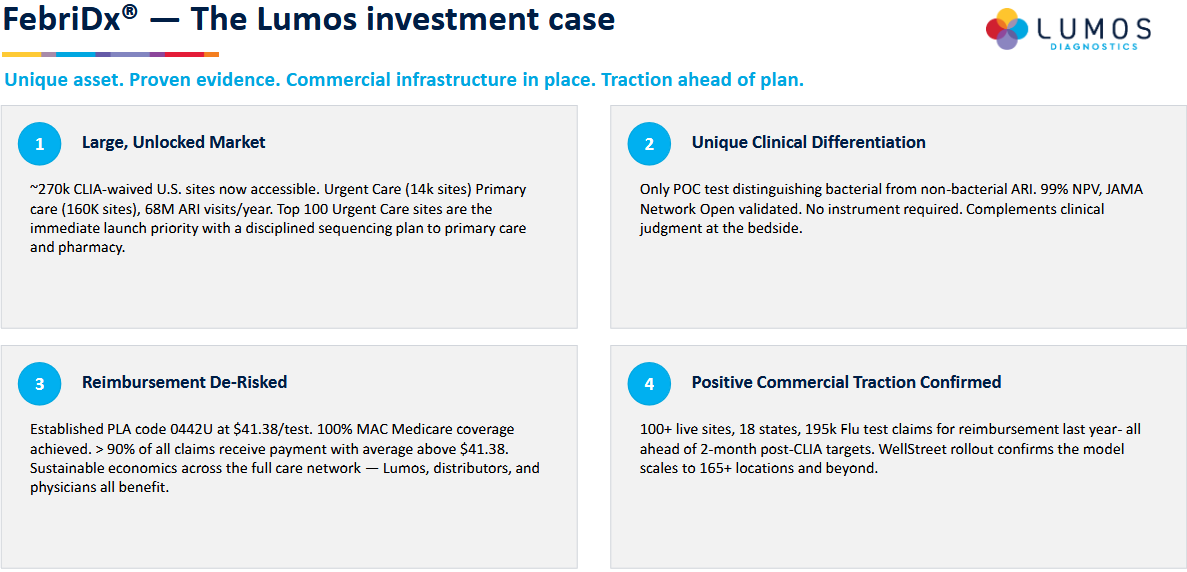

Ordinary clinic staff can now run the test at the point of care, with no lab and no specialist training, across roughly 270,000 to 300,000 sites. Urgent care clinics, GP rooms, pharmacies, community health centres.

The reachable patient pool grew to about 80 million respiratory infections a year, and the market opportunity cleared US$1 billion. That’s a 15-fold step up the whole investment case was built on.

The commercial engine is built and running. This is the part February could only promise. From here it’s the part that decides everything.

Lumos has lined up four partners to drive the US rollout, each with its own job. PHASE Scientific holds the exclusive six-year distribution deal and pushes product through the big medical wholesalers Henry Schein and McKesson. AcuityMD mines insurance claims data to aim the sales effort at the clinics with the heaviest respiratory traffic and the friendliest payer mix.

PRO-spectus walks every new site through the reimbursement paperwork so they get paid from day one. MTMC Health puts the reps on the ground.

Management calls the playbook Push, Pull, Prove. It’s pointed first at the Top 100 urgent care chains, which between them control about 40% of all sites in the country. The design is about leverage. Win a chain once, and you win all of its sites at once.

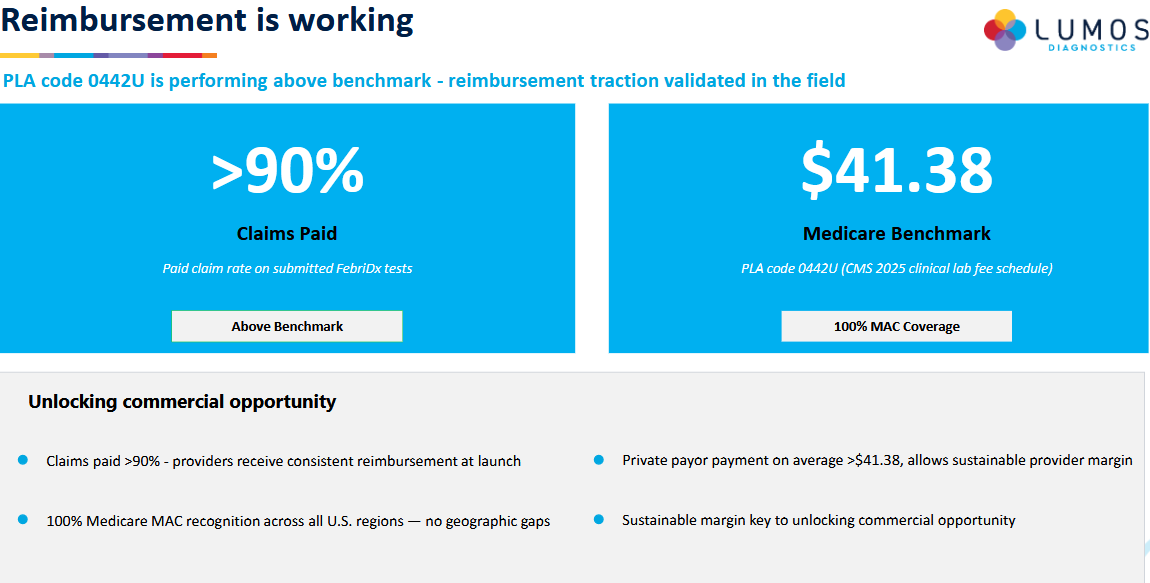

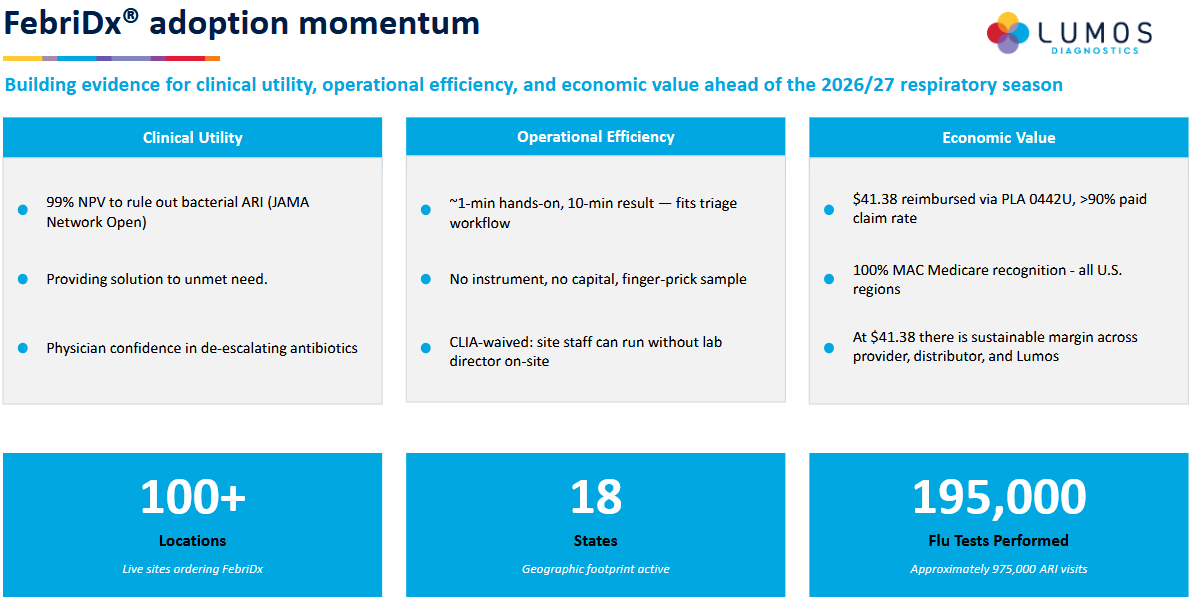

Reimbursement is working in the field, the milestone nobody cheers. A brilliant test that no one gets paid to run goes nowhere. FebriDx is reimbursed through its own billing code, PLA 0442U, at US$41.38 a test under the 2025 Medicare schedule.

Lumos now has that code recognised by every Medicare administrator in every US region. More than 90% of the claims it submits are getting paid.

Hold onto that last figure. It means the numbers work for the clinic, the distributor and Lumos all at once, which is what makes a doctor comfortable reaching for the test again next week. Private insurers are the next leg, and that push is already underway.

FebriDx sales are ramping up

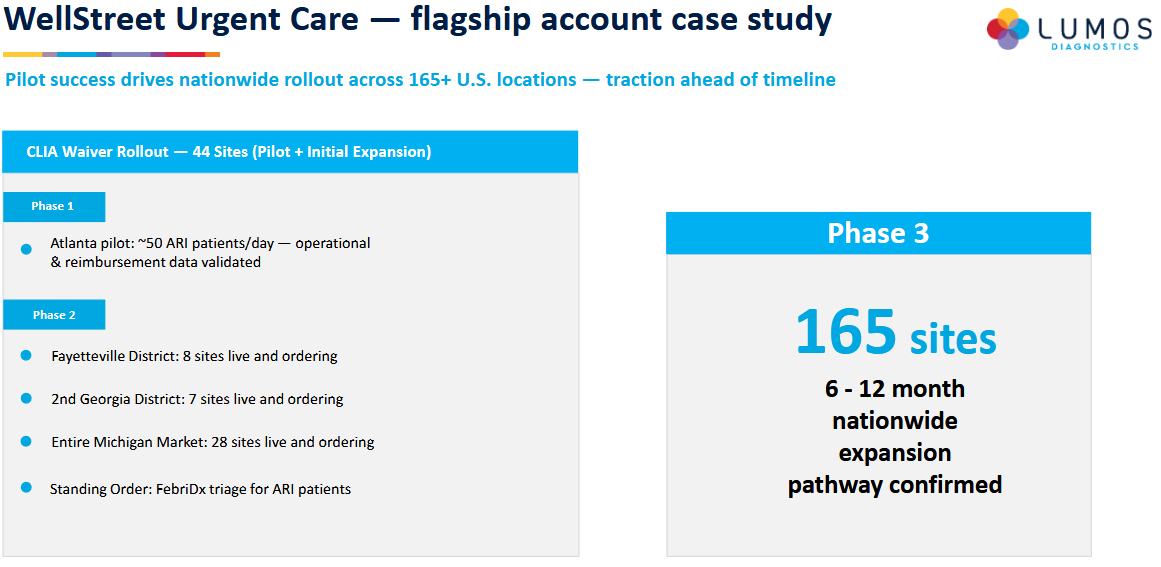

The flagship account is scaling faster than the timetable.

WellStreet Urgent Care is the live proof of concept. It’s gone from a single pilot site to 44 live locations in a matter of weeks. Eight in the Fayetteville District, seven in a second Georgia district, 28 across Michigan.

The original pilot was already seeing around 50 respiratory patients a day. Management says there’s a clear path to WellStreet’s full network of 165-plus sites over the next 6 to 12 months.

Two months on from the waiver, Lumos counts more than 100 live sites ordering across 18 states, ahead of its own post-launch targets. This is an important leading metric for future order flow.

It’s climbing into the teeth of the quiet summer, when respiratory illness sits at its seasonal low. The momentum is showing up before the demand has even arrived.

So why has the stock halved?

A self-inflicted wound. Here’s the twist. It’s the bit that frustrates, and if you’re hunting an entry, the bit that excites.

Management decided to raise money as they announced the CLIA waiver, before the market had even had a chance to reprice for the good news. The placement priced at 22.5c, when the stock had been trading with a 3 in front of it only weeks before.

Let the news breathe for a week or two and they were likely raising in the 30s, maybe knocking on 40c.

Instead the raise gave the book an offered tone, and the placement created a low instead of the high. We won’t hammer them too hard for it. Raise timing is tricky.

The consequence is a share price stuck in the bargain bin for reasons that have nothing to do with how the business is travelling. The dilution is done, the cash is in the bank, and the stock trades as though the CLIA waiver failed instead of passed.

That gap, between a company tracking ahead of plan and a price marked for failure, is too obvious to ignore in the ASX biotech sector where failed hurdles abound.

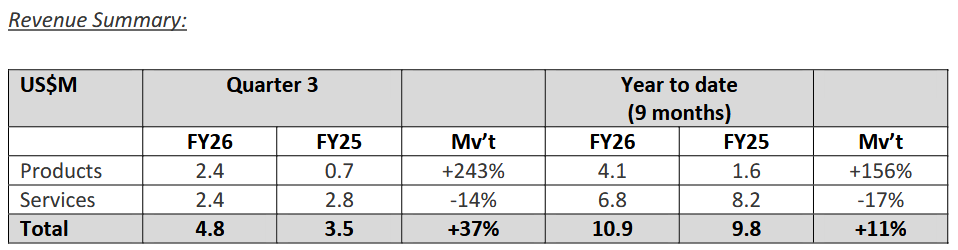

The financials

Lumos reports in US dollars. The freshest hard numbers are the Q3 FY26 quarter to 31 March 2026.

Revenue jumped 78% on the prior quarter, and FebriDx is now the bulk of product sales after the old ViraDx line got dropped. The services dip is a timing quirk from a lower amortisation rate on the Hologic licence. The customer’s still there.

Now the line under all of it. Cash. Lumos went into April with US$1.1 million in the bank. That’s why the balance sheet had to be rebuilt, and it was.

The approval switched on a wave of milestone cash. At Lumos, regulatory wins are wired straight to payments. The waiver released US$5.0 million from its US distribution partner PHASE Scientific and US$0.5 million from BARDA, the US government’s biomedical research agency. A separate paediatric study milestone added another US$0.72 million on top.

Call it US$6.2 million landing off the back of one approval, and not a dollar of it dilutive. For a company this size, that’s a serious top up to the war chest at the moment it needs to bankroll a launch.

Post-quarter the company closed a $20.0 million placement at $0.225 and a share purchase plan.

The price of that rescue is some dilution. Shares on issue now sit near 944 million. The market cap at 11.5c is about $100 million.

Minimum order quantities under the PHASE deal point to something like US$80 million of annual revenue, 65% gross margins and ballpark US$27 million of EBITDA.

We expect gross margins can grow into the 80%+ range with scale. Additionally, these are just minimum quantities in just one deal in one jurisdiction.

That’s the prize.

Outlook and catalysts

The next big catalyst is seasonal. FebriDx demand tracks the US respiratory season, which builds from November and runs through March. Lumos has launched into the quiet summer, laying the distribution rails and proving reimbursement before the wave hits.

So expect a slow ramp now, and the proper demand test from late 2026.

Q4 FY26 quarterly, due late July

The first clean read on post-waiver cash burn, and the telling FebriDx reorder rates. This gives us the indication of real end customer demand. Repeat orders mean the test is sticking, one-off stocking orders could mean demand is sluggish.

More than the numbers themselves, look for management commentary, especially in regards to the start of FY27 and the launch of new sites. It’s still all about those leading indicators.

In particular watch for data on the WellStreet scale-up. The march from 44 sites toward the full 165-location network can give us insight into the value and ease of use of the test. Watch the pace of new districts switching on. We want to see easy and rapid growth.

Private payor wins

Medicare is already locked, paying more than 90% of claims. Commercial insurers are the next leg, and each one widens the paying market.

Watch for any announcements about new private payers jumping on board. This may take time, but will be a valuable widening of the achievable total market.

Paediatric submission

The BARDA-funded study in children aged 2 to 12 runs about 12 months, carries US$6.2 million in total milestones (about US$1.9 million already banked), and opens a wider label.

Kids get sick a lot. They get the flu about 2 to 3 times the rate of adults, depending on which study you choose. They can also be more vulnerable, as their immune systems are still developing.

This 2 to 12 bracket could be a substantial boost to order volumes, and we currently have no reason to think it should be knocked back. Any announcements around the paediatric approval could be market moving.

Recommendation

Our thesis is tracking well on the fundamental milestones. The waiver landed. The market is 15 times bigger. The science holds and the reimbursement pays on more than 90% of claims.

And the selloff that followed is a great opportunity.

The ramp is largely de-risked already. US$317 million of contracted PHASE minimums underwrite the demand side, and management flagged early order momentum on the June call.

At 11.5c and about $100 million, you’re buying a validated US$1 billion opportunity at the price a mistimed raise handed you. This is fantastic buying for an investor who can carry the funding risk into the 2026/27 season.

We rate Lumos Diagnostics (ASX:LDX) a High-Conviction Buy. The July quarterly and WellStreet reorder data should be closely watched. This is one slipping under the radar, and that’s exactly when you want to be early.

Size appropriately. This is still a small-cap biotech, and we expect volatility to remain high.

Technicals

The technical setup rates a special mention. The LDX share price has fallen hard from the mal-formed head and shoulders pattern bashing against the low 30’s. But it’s held up perfectly on solid support around the 10 cent mark.

This is an area that has seen plenty of speculation, as both support and resistance. Given the risk/reward profile here, the technical pause looks compelling. A tight stop can be utilised below the recent lows to manage risk.

We maintain a buy-up-to price of $0.30 and a sell-above price of $0.60. Of course it may take time for the company to reach these milestones, but given we are in the sales ramp-up as we speak, there is certainly potential to hit these numbers.

We are aiming at a 2 to 3 year horizon.

Until next time, happy investing.

Izaac Ronay

Sign up to the Explosive Growth portfolio, and follow Izaac Ronay and The Markets IQ on LinkedIn.

Izaac is a broker and trader with Vitti Capital. He brings over 10 years of trading experience with top-tier global trading houses and 20 years of experience analysing and investing in ASX listed equities.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital — including the author of this report — may hold positions in Lumos Diagnostics (ASX:LDX) or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.

The analyst(s) responsible for preparing this research note certify that the views expressed in this report accurately reflect their personal views about Lumos Diagnostics (ASX:LDX) and its securities. No part of their compensation is, or will be, directly or indirectly related to the specific recommendations or views expressed herein. The analyst(s) and/or their associates may hold an interest in Lumos Diagnostics (ASX:LDX).