Rare Earth Elements: Seventeen Metals, One Chokehold

General advice only — prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

On 7 September 2010, a Chinese trawler captain rammed two Japanese coastguard vessels near a cluster of uninhabited rocks in the East China Sea.

Japan arrested him. Beijing demanded him back. Tokyo held firm.

Two weeks later, customs officials in Chinese ports stopped loading rare earth shipments bound for Japan. No announcement. No official ban. The cargo just sat on the docks.

Within days, Japan folded and released the captain. The shipments stayed frozen for almost two months anyway, just to make the point. And over the following year the price of dysprosium rose close to tenfold.

One fishing boat. One arrest. One commodity market that turned out to be a loaded weapon.

Fifteen years later, most investors still can’t explain how that weapon works. China fired it again last year, and this time it aimed at everyone. If you own any of the rare earth names on the ASX, or you’re circling them, you need to understand the machine underneath the headlines first.

Let’s start with the lie in the name.

Rare earths aren’t rare, and that’s the first trap

There are 17 rare earth elements. Fifteen lanthanides plus scandium and yttrium, sitting in that orphaned row at the bottom of the periodic table everyone ignored in school.

Four of them are named after a single Swedish village. In 1787 an army lieutenant pulled a strange black rock out of a quarry near Ytterby, and chemists spent the next century pulling new elements out of it. Yttrium, ytterbium, terbium, erbium. One village, four elements. No other place on Earth has that honour.

Here’s the first surprise. Cerium, the most common rare earth, is about as abundant in the Earth’s crust as copper. You’re standing on rare earths right now.

The hard part is finding them concentrated enough to mine, then prising them apart. The 17 elements are chemical near-twins. They sit together in the same minerals and behave so alike that splitting them is one of the nastiest jobs in industrial chemistry.

That leads to the second surprise. Most of what comes out of a rare earth mine is close to worthless.

A typical deposit is dominated by cerium and lanthanum. Both sell for a few US dollars a kilogram, when they sell at all. The money sits in a thin slice of the basket.

Four elements pay for everything.

Neodymium and praseodymium, NdPr in industry shorthand, plus the heavy pair of dysprosium and terbium. They make up a small share of the tonnes and the bulk of the revenue at almost every deposit on Earth. They’re the ingredients of the strongest permanent magnets we know how to make, and those magnets sit inside every EV motor, wind turbine, missile fin and robot joint on the planet.

So when a company trumpets its ‘total rare earth oxide’ resource, train yourself to ask one question. How much of that is NdPr and heavies? The answer separates orebodies from fancy dirt.

Which raises the obvious follow-up. If the stuff is everywhere, how did one country end up controlling it?

How China bought a monopoly with pollution

In 1992 Deng Xiaoping said the quiet part out loud. ‘The Middle East has oil. China has rare earths.’

At the time it sounded like a boast. It was a plan.

Through the 1960s, 70s and 80s the centre of the rare earth world was a single mine at Mountain Pass, California. Then its wastewater pipeline kept rupturing, spilling radioactive fluid across the Mojave Desert. Regulators closed in, costs climbed, and in 2002 the mine shut.

China was happy to take the business, and the mess that came with it. Rare earth ores travel with thorium, a radioactive hitchhiker. Separation burns acid in industrial quantities. Outside Baotou in Inner Mongolia sits a tailings lake of black sludge roughly ten square kilometres across. You can see it from space.

That was the trade. The West outsourced the pollution. China collected the market.

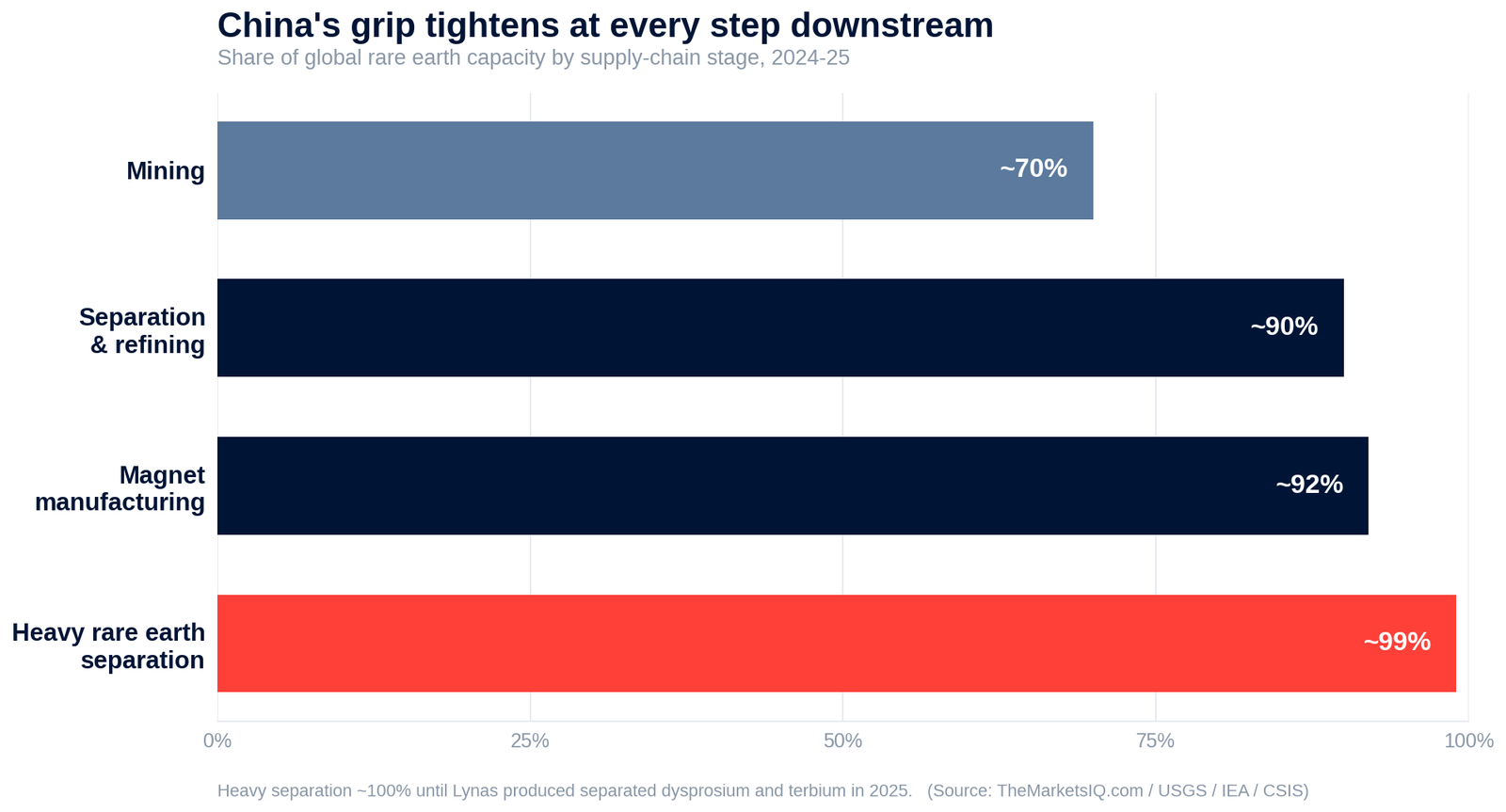

Today China mines about 70% of the world’s rare earths. It refines and separates about 90%. It makes more than 90% of the high-performance magnets. And until 2025 it controlled close to 100% of heavy rare earth separation.

The grip tightens at every step downstream.

Source: TheMarketsIQ.com / USGS / IEA / CSIS

It gets darker.

Around half of China’s heavy rare earth feedstock doesn’t come from China at all. It comes from ionic clay mines in Kachin State in northern Myanmar.

A war zone.

In late 2024 the Kachin Independence Army seized the mining region, and feedstock has been hostage to that conflict ever since.

So the most strategically sensitive metals in the Western arsenal start their journey in territory held by a rebel army, then pass through one country’s processing plants.

To see why that’s so hard to fix, you need to look at the machine itself.

A staircase China owns from the middle up

Picture the supply chain as a staircase with seven steps.

Mine the ore. Concentrate it. Crack it with acid and heat. Separate the elements. Convert the oxides to metal. Alloy the metal. Press and magnetise it into a finished magnet.

Digging the ore is the easy bit, and the cheapest. Each step above it adds more value, demands more know-how and has fewer players.

The brutal step is the fourth.

Separation runs on solvent extraction, where the mixture passes through chains of mixer-settler cells and each cell nudges the purity a fraction higher. Getting one element to 99.9% can take hundreds of stages running around the clock for weeks. The recipes are tuned to each individual orebody, and the people who can tune them are nearly all in China.

Step five is even more lopsided. Around 90% of the world’s capacity to turn rare earth oxides into metal sits inside China.

And in December 2023 Beijing banned the export of the separation and magnet-making technology itself. Sit with that for a second. Selling the product was still allowed. Selling the ability to make it was not.

For an investor the lesson is blunt.

Tonnes in the ground are the easy bit.

An orebody without a separation route is a science project. When you look at any rare earth developer, the first question isn’t grade or tonnage. It’s where the separation happens, and who owns that plant.

We’ve already seen what happens when the country that owns those steps decides to use them as a weapon.

What happens when the tap turns off

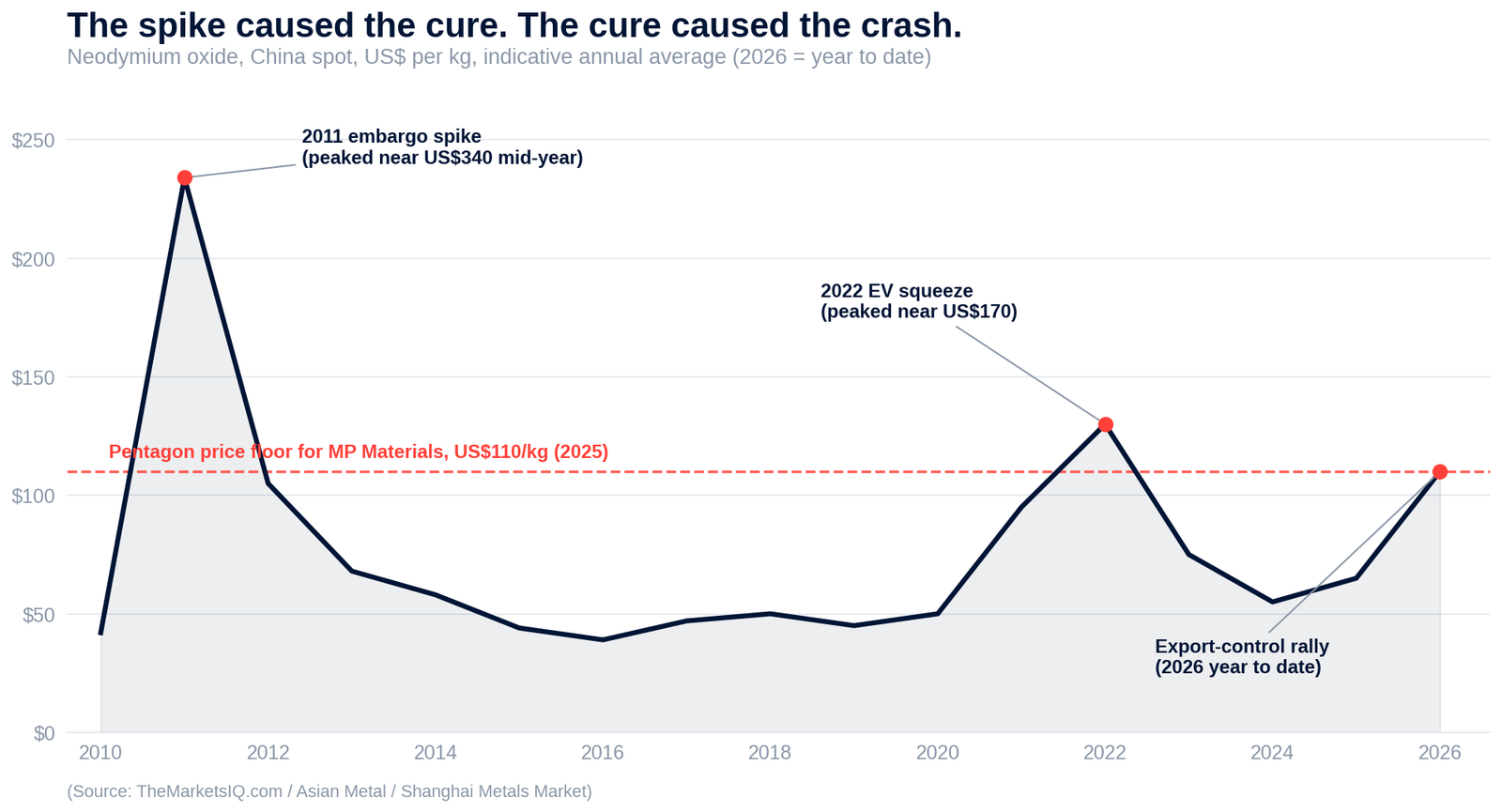

Go back to 2010. The unofficial embargo on Japan set off a global scramble, and some rare earth prices rose as much as tenfold over the following year.

Investors did what investors do. Molycorp floated at US$14 to reopen Mountain Pass and ran past US$70 within a year. Lynas Rare Earths (ASX:LYC) traded above $2 on the ASX. The story wrote itself. The West needs mines, here are the mines.

Then three things happened, in order.

Manufacturers engineered around the scarcest inputs, cutting dysprosium loadings and redesigning products. New supply arrived into a falling market. And in 2014 the WTO ruled against China’s export quotas, so the official restrictions vanished and prices collapsed.

Molycorp went bankrupt in 2015. Lynas fell below 5c, a drop of about 98%, and survived on a debt restructure and stubbornness.

The spike caused the cure. The cure caused the crash.

Source: TheMarketsIQ.com / Asian Metal / Shanghai Metals Market

Hold that cycle in your head, because last year the game restarted at a far bigger scale.

In April 2025, retaliating against US tariffs, China put export licences on seven rare earths, including dysprosium and terbium, and on the magnets containing them. Within weeks the licence queue had become a chokehold. Ford halted production lines for want of magnets that cost less than a dinner for two. A US$40,000 car, stopped by a US$30 part.

A June framework deal eased the queue.

Then in October Beijing escalated, claiming licence authority over any product, made anywhere, containing more than 0.1% Chinese rare earth content. Washington threatened 100% tariffs in response. At the leaders’ meeting that followed, China agreed to suspend the October rules for a year.

A year. That clock runs out late 2026, and nobody has dismantled the weapon. It’s been holstered.

Meanwhile Washington stopped pretending the free market would solve this. The US Defence Department took a stake in MP Materials (NYSE:MP), the company that revived Mountain Pass, and guaranteed it US$110 a kilogram for NdPr for ten years. Spot was sitting near US$60 at the time.

Apple followed with a US$500 million magnet supply deal.

Read that again. The Pentagon agreed to pay nearly double the market price, for a decade.

That’s the birth of a two-tier market. One price set in China, where supply is policy. A second, higher price for non-Chinese material, set by governments that have decided security is worth a premium.

Two prices for the same molecule. The gap between them is where the investment case lives, but only if demand holds up its end.

The demand wave you can’t substitute

Every electric vehicle with a permanent magnet motor carries a couple of kilograms of NdFeB magnet. We wrote about the demand acceleration in The Great EV Comeback, and the Gulf war has poured fuel on it since, as we warned it would when oil’s chokepoints went from theory to live ammunition.

A single direct-drive offshore wind turbine carries several tonnes of magnets in its nacelle (outer cover).

Then there’s defence, where the numbers stop being abstract.

417 kilograms. The rare earth content of one F-35.

More than 4 tonnes. One Virginia-class submarine.

Around 2.3 tonnes. One Arleigh Burke destroyer.

There’s no substitute at the performance level these systems demand. Ferrite magnets are cheap but weak. Induction motors work, Tesla has used them, but they cost you range and efficiency, which is why most EV makers keep at least one permanent magnet motor per car. The thrifting tricks, like grain-boundary diffusion to cut dysprosium content, have already been squeezed hard.

And a wildcard is arriving. Humanoid robots are dense with small precision motors, and the estimates run at 2 to 4 kilograms of magnets per robot. If even the cautious forecasts for that industry land, it’s a second EV-sized stream of demand.

Magnet demand has compounded at high single digits for years and nothing on the horizon slows it. The strain lands on exactly the elements China restricted.

Which brings the story home, because the ASX hosts more of the Western response than any other exchange.

The ASX names doing the West’s homework

Run through the local roster in order of how far up the staircase each one has climbed.

Lynas is the only producer of separated rare earths at scale outside China, mining Mt Weld in WA and separating in Malaysia. In 2025 it produced separated dysprosium and then terbium, the first commercial heavy rare earth supply outside China in decades. It’s building cracking capacity in Kalgoorlie and a heavy separation plant in Texas with Pentagon funding.

Iluka Resources (ASX:ILU) is building Australia’s first fully integrated refinery at Eneabba in WA, backed by about $1.65 billion in Commonwealth loans. Its edge is a stockpile of monazite, a rare-earth-rich byproduct of decades of mineral sands mining, already dug up and sitting above ground.

Arafura Rare Earths (ASX:ARU) carries a Commonwealth support package of about $840 million for its Nolans project in the NT, aimed at NdPr.

Australian Strategic Materials (ASX:ASM) already works on step five of the staircase. Its metals plant in South Korea turns oxides into the metals and alloys magnet makers buy, one of the few facilities outside China that can. The Dubbo project in central NSW is the orebody meant to feed it.

Hastings Technology Metals (ASX:HAS) is developing Yangibana in the Gascoyne, an ironstone deposit where NdPr makes up a fat share of the basket.

Northern Minerals (ASX:NTU) owns Browns Range in WA, one of the few heavy rare earth deposits outside China and Myanmar. Canberra forced a Chinese-linked fund to sell down its stake in the company. It’s also been hacked. When a microcap attracts that much unwanted attention, the asset means something.

A cluster of ASX-listed juniors, Meteoric Resources (ASX:MEI) and Brazilian Rare Earths (ASX:BRE) among them, hold ionic clay deposits in Brazil. The same geology behind southern China’s heavy rare earth supply, without the war zone attached.

Then there’s the urban mine.

Decades of dead hard drives, air conditioners, wind turbines and EVs are reaching the scrap heap with their magnets still inside, and less than 1% of those rare earths get recovered. Ionic Rare Earths (ASX:IXR) attacks that gap from both ends. Its Makuutu project in Uganda sits in the same ionic clay geology that supplies China’s heavies, and its plant in Belfast turns dead magnets back into separated magnet-grade oxides.

A heavy rare earth supply chain with no war zone and no thorium attached. That’s the pitch, and Apple’s recycled-magnet deal with MP Materials shows the demand side agrees. The cheapest new mine might be the scrap bin.

Before any of these names go near your portfolio, run three checks.

First, the separation route. Who turns the concentrate into sellable oxides, in which country, and is that plant built, funded or imaginary?

Second, the basket. Ignore the headline resource number and price the NdPr and heavies inside it. Standard mining yardsticks mislead in this market, the same way we showed AISC flatters and deceives in gold.

Third, the funding. These projects cost more than junior miners can raise on market. A government on the register is both a validation stamp and your best protection against endless dilution.

So how do you put all of this to work?

The road from here

Three traps, then three signals.

Trap one is the tonnage headline. A billion tonnes of rare earth resource with a weak NdPr and heavies share is a billion tonnes of expensive dirt. Price the basket, never the total.

Trap two is buying the spike. The 2011 chart is the most important chart in this market. Restriction announcements create rallies that price in permanence, and history says the restrictions bend. Demand gets engineered down, supply gets dragged forward, and the latecomers wear the round trip.

Trap three is reading the price as a market signal at all. NdPr is now priced by politics at both ends. Beijing decides how much supply exists. Washington decides what the floor is worth. The spot price in between tells you less than it used to.

Now the signals worth watching.

Watch Chinese licence behaviour as the truce expires late this year. The October rules were suspended, never cancelled, and how Beijing handles that deadline tells you whether the weapon comes back out.

Watch the spread between Chinese spot and the Western floor. The US$110 NdPr floor is the first honest statement of what secure supply is worth. If more governments and manufacturers sign deals at that level, the two-tier market hardens and the non-Chinese producers get paid the premium price.

Watch the downstream builds, the separation plants and magnet factories, because capacity there has been the bottleneck all along. A commissioning date moving on schedule matters more than any drill result.

For 15 years this was a sleepy corner of the mining market that punished everyone who touched it. Now both superpowers have decided it’s a matter of national security, and both are writing cheques. The companies standing on the right steps of the staircase have something close to guaranteed customers for the first time in the industry’s history.

The dirt was never the prize. The chokepoints were.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital — including the author of this report — may hold positions in the companies mentioned or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.