Maas Group (ASX:MGH) - Synergies Case Study

General advice only – prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

If you spend enough time reading merger and acquisition announcements on the ASX, you’ll find a magical word bandied about as the cure for all that ails a struggling business.

SYNERGIES.

Cue Also sprach Zarathustra. That’s the music used at the start of 2001: A Space Odyssey to convey awe and wonder.

But what does this mystical SYNERGIES word even mean?

It’s one of the most overused and least understood words in the investment space.

Check out our Synergies Deep Dive here if you haven’t already. This case study is written as an addition to the deep dive.

Let’s step through a synergies case study.

MAAS Group (ASX:MGH) is a great example of synergies, with so many acquisitions for us to look through. Their whole business strategy is around exploiting synergies. It’s beautiful and simplistic.

This is the story of how a regional operator built a vertically integrated construction machine, and how the numbers moved as it was all stitched together.

Maas Group overview

MAAS Group is a diversified Australian industrial group built around construction materials and civil delivery. It also has real estate and a manufacturing arm, but the heartbeat is the materials chain – quarries, concrete, asphalt and the logistics that move it.

The group sells into civil infrastructure, building, construction and mining demand. The edge comes from building dense hubs in a region, then feeding its own materials into its own civil jobs, while third-party sales keep the plants busy.

The Wes Maas factor

You cannot tell this story without Wes Maas. He founded the business in 2002 and grew it from one Bobcat and a tipper truck into an ASX-listed group.

Mergers and acquisitions are tough, messy work. A new owner is just as likely to screw up a business as find those elusive synergies.

That’s where management expertise is paramount. Leaders who have a history of quickly integrating new acquisitions and boosting returns are more likely to be able to do it again.

The under-discussed aspect of unlocking synergies is there’s actually an insane amount of work and expertise required.

Integration is a core strength of MGH.

The playbook has been simple. Buy assets that deepen the chain. Add scale in the same geography so depots, people and plant can be shared. Keep the best operators. Standardise systems. Maximise utilisation and internal demand.

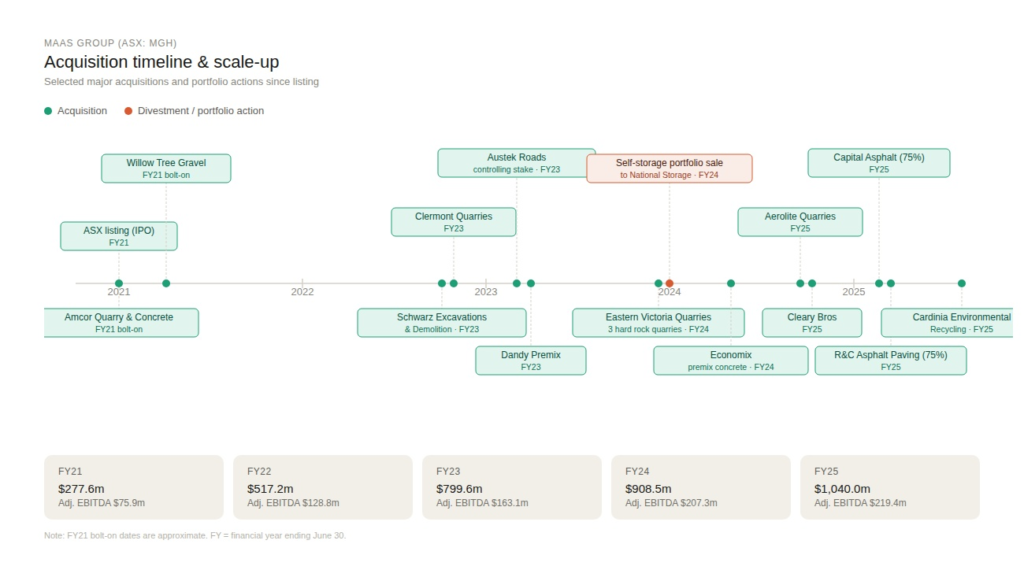

The acquisition journey

The chart below is a simplified timeline of the major platform moves from listing through to FY25. That’s one heck of an active acquisitions department.

The Maas Group synergy engine

MGH’s synergies are structural.

They are building a vertically integrated construction materials chain, then feeding it with internal demand from civil work and property activity.

That creates three repeatable levers.

First, utilisation, because you can keep plants and quarries busy with internal jobs even when external demand is patchy.

Second, margin control, because owning more of the chain reduces reliance on third-party suppliers.

Third, capital recycling, because mature assets can be sold and the proceeds redirected into higher-return materials capacity.

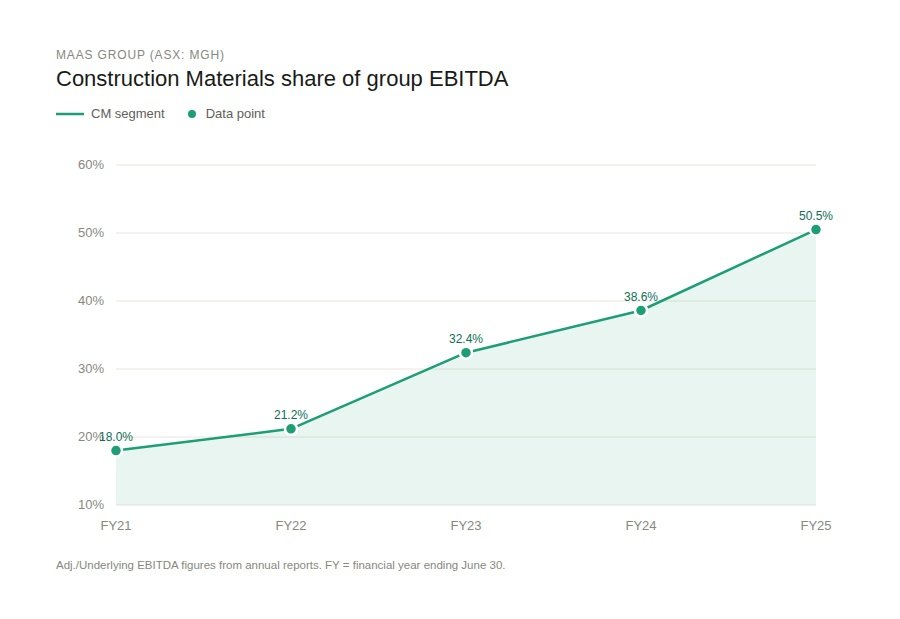

Construction Materials

This is the cleanest synergy proof in the whole MGH story. You’re looking for three things. Construction Materials growing faster than the group, Construction Materials becoming a larger share of earnings, and large intersegment eliminations.

Intersegment eliminations are basically an accounting technique for dealing with sales from one business segment to another. So, whenever you see ‘Intersegment eliminations’ in the accounts, it tells you that there could be synergies at play.

If you only look at group revenue, you miss the real story. MGH is turning into a construction materials earnings machine. By FY25, Construction Materials is half of group underlying EBITDA, up from under one-fifth in FY21.

The financial evidence of synergy

FY21

FY21 is the base camp.

Group revenue is $277.6m and underlying EBITDA is $75.9m. Construction Materials is smaller at $43.4m of revenue and $13.4m of EBITDA, but it already carries a fat margin of 30.8%.

The tell is intersegment eliminations of $26.8m. That is internal trade being removed in consolidation. It means the group is already selling to itself across segments, which is the beginning of vertical integration.

FY22

FY22 is where scale starts showing up.

Group revenue jumps to $517.2m and underlying EBITDA lifts to $128.8m. Construction Materials revenue lifts to $113.4m and EBITDA to $27.3m.

The margin drops to 24.1%. That can happen when you grow fast and you are still integrating. The more important number is Construction Materials share of group EBITDA rising to 21.2% and eliminations rising to $43.9m. Internal trade is expanding with scale.

FY23

FY23 is the traction phase.

Group revenue lifts to $799.6m and underlying EBITDA to $163.1m. Construction Materials revenue more than doubles to $243.4m and EBITDA climbs to $52.0m.

Construction Materials now drives 31.9% of group underlying EBITDA. Eliminations rise again to $57.8m.

The group is increasingly its own customer. SYNERGIES.

FY24

FY24 is the maturity test.

Group revenue moves to $908.5m and underlying EBITDA to $207.3m. Construction Materials revenue lifts to $385.9m and EBITDA to $80.2m.

Construction Materials share of EBITDA rises to 38.7%. The EBITDA margin holds around 20.8%, which is impressive given the scale increase. Eliminations are still chunky at $60.4m. That supports the thesis that MGH is not just buying assets, it is knitting them together.

FY25

FY25 is the punchline.

Group revenue passes the billion mark at $1,040.0m. Underlying EBITDA is $219.4m. Construction Materials revenue hits $535.7m and EBITDA hits $110.7m.

Construction Materials is now 50.4% of group underlying EBITDA. That is a radical mix shift in four years. Eliminations fall to $49.7m, but that is still huge in absolute terms. The integrated engine is now big enough to change the whole group profile.

The value realisation

Maas build strong value via strongly synergistic integrations. In early 2026 the company announced it would be divesting its Construction Materials division for a cool $1.7 billion. For context, the market cap of the whole business was about $2 billion right before the deal was announced.

While Construction Materials is by far the most attractive part of the business, there are still several other divisions which will be retained, contributing about half of the EBITDA.

Their next move is into AI and data centre infrastructure. We’d bet the growth will be fuelled by a healthy string of acquisitions. If Wes Maas is still at the helm, we’ll more than likely see those synergies continue to hit the bottom line.

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.

Directors, staff, or clients of Vitti Capital may hold positions in Maas Group (ASX:MGH) or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.