Explosive Growth Portfolio Update December 2025

A Powerful Launch

General advice only – prepared for Wholesale/Sophisticated/Professional Investors. See full disclaimers below.

In the spring, we launched the Explosive Growth Portfolio to identify small‑cap innovators quietly wiring the future.

We launched the Portfolio with a simple goal.

To find asymmetric opportunities with macro tailwinds and company-specific edge. Accept volatility and position for catalysts.

A few months in, the picture is bright.

This portfolio is doing exactly what it was built to do.

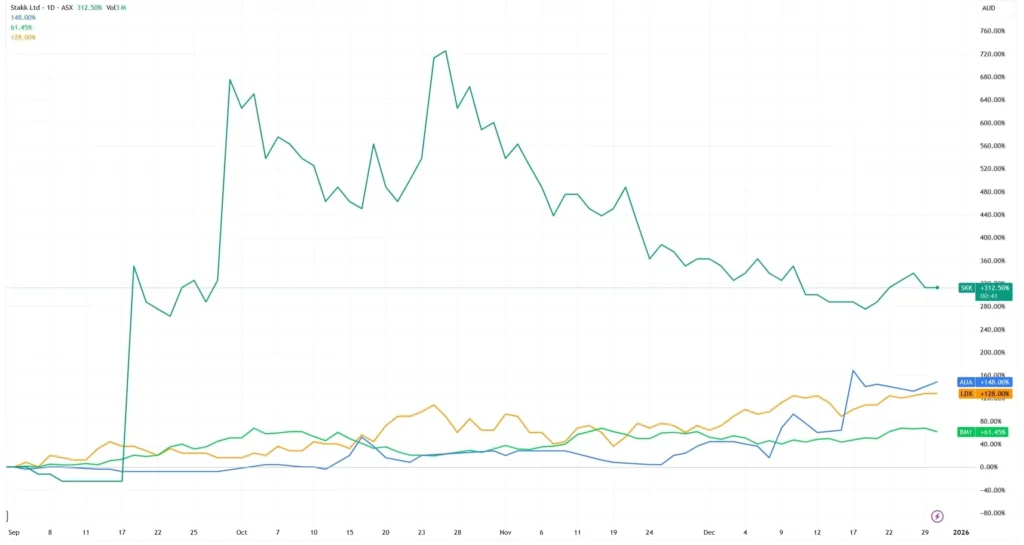

Across four positions, the portfolio is up 180% in aggregate, or 45% on average, since initiation. Annualised, that’s just over 168%.

Not every stock is green. And that’s part of the strategy. When positioning for Explosive Growth, we have to accept some steep pullbacks on the way up, and a few losers to boot. That’s just the nature of taking higher-risk, higher-return opportunities.

Let’s run through each position and what’s changed.

Lumos Diagnostics (ASX:LDX)

Lumos Diagnostics (ASX:LDX) remains the standout performer.

Since initiation at $0.13, the stock is now trading at $0.28. That’s a 115% gain. And again, this move has happened before the main event.

The real inflection point is still ahead, the CLIA waiver.

That approval is the gate that unlocks full commercial scale in the US. Without it, FebriDx adoption is constrained. With it, FebriDx moves into urgent care, primary care, and high-throughput clinical settings where volume could occur effortlessly.

This is also what activates the full value of the Phase Scientific agreement, worth ~$487 million (US$317 million) in minimum order quantities over the first six-year period. The distribution is there. The commercial framework exists. CLIA is what allows that deal to reach full potential.

With all seven Medicare contractors now reimbursing at US$41.38 per test, barriers to adoption have largely fallen, and urgent‑care chains are beginning pilot programs.

Combined with a new partnership for AcuityMD’s data analytics platform and a Baltic distribution deal, LDX is delivering strong progress on several fronts.

So, it’s no surprise to see the price strong, leading into the main event of the CLIA waiver decision.

Ballard Mining (ASX:BM1)

We initiated coverage on Ballard Mining (ASX:BM1) on 7 Oct 2025 at $0.68. After a sharp rally through November, the stock has been largely sideways.

The muted share price belies a torrent of positive operational news. The company completed its 80 km Phase 1 drilling program, reporting high‑grade hits such as 3 m @ 64 g/t gold and 8 m @ 11 g/t while identifying 35 new structural targets at Mt Ida.

A $20.6 million strategic placement at $0.55 per share has filled the war chest for deep drilling.

Our thesis was that Ballard could rapidly grow its resource base and convert its Mt Ida discovery into a long‑life reserve. That process is on track. Management is targeting a 400–500 koz maiden ore reserve by mid‑2026, and Phase 2 regional drilling will commence early next year.

The share price has underperformed, but the potential catalysts remain compelling. Watch for potential resource updates in the March quarter.

Audeara (ASX:AUA)

When we initiated Audeara (ASX:AUA) on 7 Nov 2025 at $0.032, we described the company as a hearing‑technology platform disguised as a headphone maker.

Over the past two months, that identity shift has accelerated. Audeara secured NMPA certification in China for its personalised‑hearing technology, clearing the path for a commercial launch via China’s leading e‑commerce channels.

A record $560k purchase order lifted year‑to‑date wholesale revenue to $1.75 million, up 50 % on the prior period.

The company also signed a chip‑level AI licensing deal with OPTEK Microelectronics, embedding Audeara’s algorithms into audio chips on a fee‑per‑chip basis. This is a potentially massive deal, which has led to a wave of speculative positioning in this nano-cap.

These wins have driven the share price to roughly $0.062, producing a 87% gain (600%+ annualised).

The market is beginning to recognise that Audeara’s future lies in recurring licensing revenue, not hardware.

Key catalysts ahead include the February delivery of the record order, the China launch under Eastech’s partnership, and further licensing deals.

Stakk (ASX:SKK)

Infrastructure stories are rarely smooth and Stakk (ASX:SKK) remains the laggard on price. It’s worth noting, however, that it’s also the newest of the bunch, with coverage launching on December 2nd.

From initiation at $0.38, the price has retraced to $0.033, a 13 % decline, despite the company continuing to land significant agreements.

Earlier this month, the SKK announced a multi‑year master services agreement with Panacea Financial, a physician-focused U.S. neobank backed by Peter Thiel’s Valar Ventures.

Under the deal, Stakk’s mobile image capture, optical character recognition, and document orchestration tools will power Panacea’s deposit‑acceptance system.

Revenue will be generated through a monthly platform fee and usage‑based transaction fees, with billing beginning in January 2026.

The sell‑off reflects the hangover from a 450 % rally earlier in 2025 rather than any deterioration in fundamentals.

Stakk remains a unique, pure‑play on the embedded‑finance infrastructure layer, and the Panacea deal provides another proof point that its technology scales across verticals.

Upcoming catalysts include the January cash‑flow report (which should show accelerating SaaS revenue) and additional enterprise contracts.

In Summary

Two stocks are up more than 100%.

One is flat.

One is down.

And the portfolio as a whole is still delivering ~170% annualised performance.

LDX hasn’t hit its regulatory trigger yet.

AUA has only just reshaped its model.

BM1 is still exploring.

SKK is still embedding.

Volatility will remain, and 2026 holds all the promise of an even more exciting year.

It’s a solid start. We can’t wait to share our next picks with our readers. There are plenty of small cap ASX stocks sitting on potentially massive catalysts.

You can check out all of our Explosive Growth writeups, along with CEO interviews at TheMarketsIQ.com.

Explosive Growth Portfolio Picks Daily Price Chart (Source: Tradingview)

This publication has been prepared by The Markets IQ, a division of Vitti Capital Pty Ltd (ABN 13 670 030 145), which is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence 518031. This report is for general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial advice or a recommendation to buy, hold, or sell any security. You should consider whether the information is appropriate in light of your circumstances and obtain professional advice before making any investment decision. This report is intended solely for wholesale, sophisticated, or professional investors within the meaning of the Corporations Act 2001 (Cth).

Any views, probabilities, valuations, technical levels, or forecasts expressed are strictly the opinions of the authors as at the date of publication, based on publicly available information and assumptions which may change without notice. They are illustrative only and not predictive of future outcomes. Past performance is not a reliable indicator of future performance.Directors, staff, or clients of Vitti Capital may hold positions in Lumos Diagnostics (ASX: LDX) or related securities at the time of publication. Such holdings may change without notice. Vitti Capital applies internal controls to manage potential conflicts of interest; however, readers should assume that conflicts may exist.