NVDA Meltdown is a

Warning Shot for Big Tech Investors

Nvidia (NASDAQ:NVDA) has had a rough couple of days in the share market, down 22%. The whole AI sector is down with it. This isn’t just about one company—Nvidia’s fall matters because of its outsized role in the AI economy and its massive weighting in the NASDAQ index - about 9%.

Its chips power everything from data centres to autonomous vehicles, and when its valuation wobbles, it shakes confidence in the entire ecosystem. In addition to this, its reliance on China for growth and the rising competition from Chinese chipmakers are a recipe for sector-wide turmoil.

NVDA has boomed on the back of the rise of cryptocurrency and AI. It's been one of the most hyped and heavily overvalued stocks for several years.

And it's consistently validated those valuations with astronomical growth.

It's hard to find a better success story for the past decade. Needless to say, it attracts attention when we see such a massive fall.

So, what the hell just happened? Is this the start of the next market meltdown, or just another bump in the road for growth stocks?

As with all market moves, there are big opportunities shaping up that we need to discuss and that you won't want to miss out on.

But first, let's cover what's happened so we can set the scene.

What Happened?

If you're not on top of AI chatter, you may have missed the headlines.

They're not about immigrants, Trump or the exorbitant cost of housing.

Chinese AI is storming the gates.

Companies like Baidu and Huawei are making groundbreaking advancements in natural language processing and AI-driven chip designs, while Tencent’s AI lab is leading in generative models that rival OpenAI.

Meanwhile, China’s state-backed research enables rapid AI deployment in applications like facial recognition and autonomous vehicles, giving them an edge in practical implementation.

In a matter of months, China has gone from an emerging player to a credible threat, pouring billions into tech giants like Baidu, Tencent, and Huawei. The government’s aggressive strategy includes funding, subsidies, and a well-orchestrated plan to dethrone US dominance in AI.

However, the most recent fall was more specifically related to another company.

DeepSeek.

It sounds like a cheap imitation of a muscle pain relief cream and a job and website rolled into one.

It's actually China's most recently announced weapon for supremacy in the battle against the US.

It's an open source AI language model that is said to rival the best that the US has to offer, including OpenAI's latest ChatGPT model - o1.

The scary part for US AI companies is that DeepSeek has achieved this for a fraction of the cost at about US$10 million and in just two years, a fraction of the time.

OpenAI has reportedly raised about US$20 billion so far and costs a hefty US$5 billion per year to run.

That's quite the disparity.

So what do we know about DeepHeat....ahem, excuse me, I meant to say DeepSeek.

Sure, it's a private company. Wink wink.

And the Chinese Communist Party would never steal the IP of foreign companies. After all, how can you steal something when under communism there's no private ownership?

So, as an 'independent' company is it unbiased?

That depends on your stance on things.

Ask it if Taiwan is an independent country and the answer is absolutely not. It's an integral part of China, always has been, always will be.

Why do people compare President Xi to Winnie the Pooh? No idea what you're talking about, you sound crazy to me.

What was the Tiananmen Square Massacre? No idea what you're talking about, you sound crazy to me.

OK, so the responses on the last two are closer to 'I am sorry, I cannot answer that question.'

But if anything, that's even more ominous. You can just feel the CCP's grip DeepSeek's throat.

Ask it what's wrong with Capitalism and it will give you a list of seven flaws, making capitalism sound like a veritable death march.

Ask it what's wrong with Communism, and the response is much shorter.

'Let's talk about something else.'

Concerns around integrity and bias aren't tampering a massive reaction to the new entrant.

If one company can make advanced AI software so quickly and cheaply, others might not be too far behind.

Nvidia is feeling the heat. US export restrictions on high-performance chips to China have sliced off a chunk of Nvidia’s addressable market. Meanwhile, Chinese firms are scrambling to build their own cutting-edge silicon.

The market is factoring in a potential shift in global AI leadership and a potential loss of market share for US firms.

So Are the Markets Melting Down?

What we're really trying to figure out is if this is the start of a massive crash or something much more isolated.

We need to see how important markets are reacting to know the implications.

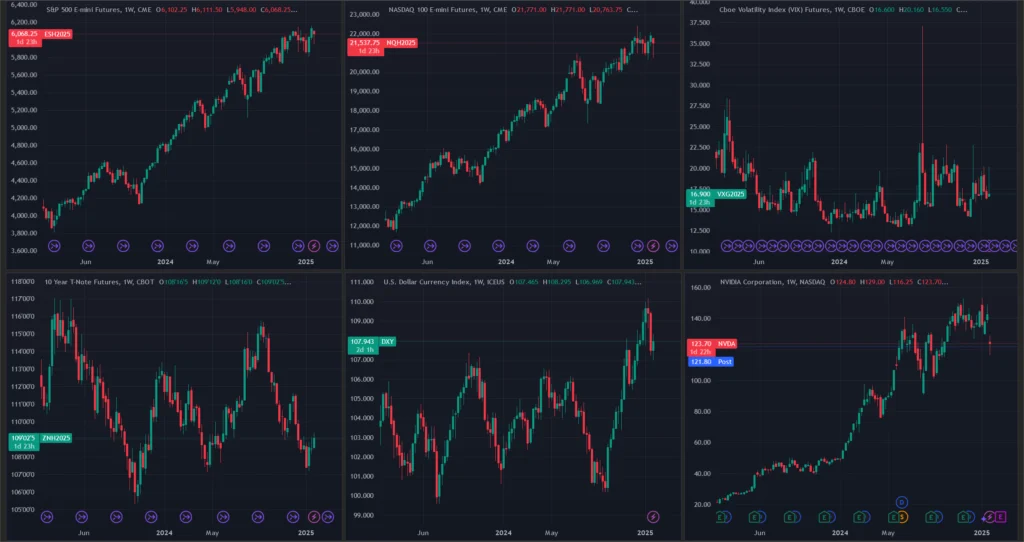

The interplay between key market indicators paints a picture of investor sentiment and economic expectations. When stock indices drop while bond yields rise, it often signals a flight to safety, with investors rotating out of growth assets. A rising VIX suggests fear and uncertainty, while a strong DXY makes US exports less competitive, putting further pressure on corporate earnings.

All of these moves played out to a limited extent. But have been mostly quickly reversed.

S&P 500 Futures (CME:ES) has shrugged off the news with a momentary and minor pullback.

Nasdaq 100 Futures (CME:NQ) took a square punch to the face, but it's still standing. AI and chip stocks have been hit hardest, but the index overall was down about 6% and had recovered most of that already.

So investors haven’t been warned off tech stocks in general, just AI stocks.

The US 10-year bond (CBOT:ZN) caught a bid tone and has remained strong, although nothing too dramatic. Some cycling into bonds suggests the market sees some risks in stocks. But it's certainly not flashing warning signs.

The S&P500 Volatility Index (CBOE:VX) is generally the best gauge of clear and present danger. To be fair, it did have a decent spike up, suggesting some fear that the stock market could crash.

But it's since come back quite a way, with the majority of the move now pared back. It also saw a bigger spike six weeks earlier when the FED changed its rhetoric around rate cuts.

The US Dollar Index (ICE:DXY) couldn't pick a direction on the news and wasn't even especially volatile.

So all of this suggests that, on the whole, the market has already forgotten it.

However, this is an important time to prepare for any secondary market reactions and subsequent news compounding on the initial story.

Markets Snapshot (Source: TradingView)

High Bond Yields and Competition

High bond yields are bad for growth stocks. During higher interest environments, investors generally pull money out of growth and high-risk assets and put it into safer plays with immediate cash flow.

This is because debt becomes more expensive, and the value of money earned in the future decreases.

Growth stocks are valued on future earnings potential, not what they’re making now. When the cost of debt is cheap, investors can borrow money to invest in growth stocks at very little cost and wait for that investment to pay off in the future.

When interest rates increase, the cost of that debt goes up, and so the value of money earned in the future decreases by comparison.

In that environment, investors pay down debts and return money to cash. They also switch stock investments from growth into stable bluechips and index funds.

Right now, the NASDAQ is priced for extremely strong growth. The market is betting that the biggest tech stocks in the US will have a phenomenal year.

That makes these valuations especially vulnerable to increased Chinese competition. It's extremely unlikely that China will rise up and take substantial market share in the next 12 months.

But there are two things to consider here.

Firstly, we've seen China emerge from nowhere to become the global leader in EV manufacturing in just a few short years. To be fair, they've been working on the technology for a long time. But its market share has heavily shifted in the last few years.

And it's not just EVs. We never used to think about Chinese automakers or know their names until recently. Now, China produces a third of all cars globally.

That's massive!

So, we know China is on a mission to take over whole industries. It's the CCP playbook for global domination.

The second thing to keep in mind is that markets are forecasting machines. They don't price assets based on current performance but on what is expected to happen in the future.

If we start to see more and more news about Chinese firms taking over the AI space, the market could react quickly and violently.

Light at the End of the Tunnel

It’s not all doom and gloom.

Where there's volatility, there's opportunity.

While the future of US AI stocks just became less certain, their current valuations a bit riskier, there are still plenty of plays in the market that will benefit from the general theme of AI without having to be building the large language models themselves.

And some of them are right here at home on the ASX.

You might have heard of NEXTDC (ASX:NXT). It's an ASX-listed data centre operator that has caught a lot of hype.

It's valued at $9.4 billion or 23X trailing revenue, despite being loss-making. The analyst consensus is for a maiden profit all the way out in FY28. But, the current valuation doesn't really start to make sense until all the way out in FY32, with a forward PE of about 15X.

So, we can safely say this one is not flying under the radar. The market is loving it, and pricing in perfection. We're sceptical that there's much upside here.

Enter Infratil (ASX:IFT), the unloved step-child to the market that can't catch a break. It's trading at $9.8 billion, which is only 3.3X trailing revenue.

So, why doesn't the market have love for Infratil?

Could it be because it's already profitable, with a trailing PE of 10.4? Or the dividend of 16.44 cents, which equates to a 1.6% trailing yield.

Infratil does more than just data centres, so it's not a directly comparable business.

It also owns renewable energy, healthcare technology and airport infrastructure.

But the growth is certainly impressive, with a 25% increase in EBITDAF reported in the recent half-year report.

The important thing is that this is an already profitable business trading at a low valuation and under the radar.

Most importantly, our demand for data storage and processing will continue to increase regardless of whether Google or DeepSeek win the AI war.

Then, some opportunities that still taking off and are completely unrelated to the whole AI theme.

Take robotics, for example. There's a company on the ASX right now building the brick walls of houses with a robotic crane arm.

They're about to launch a tasty joint venture in the US, and the contract has them standing to make big bucks.

We're talking about FBR (ASX:FBR), formerly FastBricks. They've got the backing of one of Australia's best investment houses and oldest brick makers in Brickworks (ASX:BKR).

The Hadrian X in action (Source: FBR.com.au)

And that joint venture in the US is with one of the industry titans, CRH. So they're certainly getting the buy-in from the big players who understand the industry.

The big ramp-up in production and sales is all set to take place in 2025, and we expect the profit to start building in about 2027.

If the AI theme stops dead in its tracks, we'll still need to build houses. And this is the company with the latest and greatest technology to allow that to happen more efficiently.

This isn't intended as a deep dive into IFT or FBR, and it's certainly not a buy recommendation.

We'll let you do your own research to determine if these are companies you want to own or not.

Final Thoughts

USA's unchallenged AI dominance may be coming to an end. There's certainly been a shot across the bow.

We certainly don't need to man the panic stations just yet. But this is an opportunity to think about what could play out.

If you're reviewing your portfolio and find yourself overexposed to US tech, this could be a good time to reallocate some funds.

There are plenty of opportunities flying under the radar, and you just need to start looking.

The AI boom might face turbulence, but savvy investors know that change breeds opportunity. Keep your eyes on the prize, and don’t sleep on the sectors that are about to take flight.

FBR and Infratil weekly price charts (Source: TradingView)

- ASX:FBR

- Infratil

- Robotics

- AI

- Artificial Intelligence

- Construction

- data Centers

- Next DC

- DeepSeek

- Chat GPT

- Nvidia

- Nasdaq

- Bonds

- NVDA

- ASX:IFT

- Tech

- China

- USA