CBA is Too Expensive:

Time to Reevaluate?

Commonwealth Bank of Australia (ASX: CBA) Stock Price Analysis

The Commonwealth Bank of Australia (ASX: CBA) is the undisputed heavyweight champion of ASX bank stocks. But in the last twelve months, we’ve seen its valuation become unhinged from reality.

CBA shares have surged 60% in just over a year.

And for what?

Selling the same mortgages and skimming the same interest margins? There’s no growth story here. Just a bubble inflating before our eyes.

After the 1H FY25 result update, CBA shares fell over 11% in 7 trading days. While the price has since stabilised, the fall is a warning shot for CBA holders. The correction? This could be the warm-up act.

The sharks are circling, and it’s time to sit up and pay attention.

CBA’s recent share price decline wasn’t out of the blue. The meteoric rise in valuation was dizzying, bizarre and unwarranted.

To be clear, CBA is not in financial strife. Far from it.

The result was solid, with 4.7% growth in year-on-year revenue and Earnings Per Share (EPS) up 6.6% to $3.08. The Net Interest Margin (NIM) expanded 2 basis points to 2.08%. That’s the interest margin that the bank achieves between what it borrows and what it lends.

The major problem is that single-digit growth is as much as we can expect. CBA's growth of 60% from here would be like BHP's sudden discovery of a new continent made of iron ore. Not happening.

After a series of expansion failures into complementary businesses and geographies and the debacle of the Royal Commission, the big banks are gun-shy about big expansion moves. </p

This leaves initiatives for easy and manageable activities. Margin expansion initiatives, digitisation, AI for efficiency. All the small things add up over time but don’t make for sustained double-digit growth.

Commonwealth Bank of Australia (ASX: CBA) Stock Price Analysis

For years, CBA has traded at a premium to its banking peers. But, the last 18 months of rampaging price growth have put CBA into the stratosphere.

Before its latest drop, CBA was trading at a trailing PE of around 29.6X, far above the almost 19x that WBC and NAB peaked at. It’s also well above where the banks usually trade, at about 12-16x PE.

stratosphere.Even after the fall and the increased earnings in 1H FY25, the trailing PE for CBA still sits elevated at 26.7x.

Three-year PE chart of the three largest ASX banks (Source: S&P Capital IQ)

Remember, we’re not talking about a high-flying tech stock that can easily pump out 50-100% revenue growth in a year. This is a mature, stable business.

Even outside banking, CBA’s valuation is out of step with reality. Investors are treating it as Australia’s equivalent of Apple or Microsoft—companies that dominate their sectors with strong moats and scalable global businesses. But, CBA’s business model is fundamentally constrained. It operates in a saturated market, faces rising regulatory pressures, and has minimal room for meaningful growth. The market’s blind faith in its ‘quality’ has led to a valuation that is unsustainable.

The Index Compounding Effect

One major reason CBA soared to such inflated levels was the passive investing boom. As Australia’s largest company by market cap, CBA is a heavyweight in the ASX 200, meaning super funds, ETFs, and index funds became forced buyers. The more CBA rose, the bigger its weighting in these indices, leading to even more buying. A dangerous self-reinforcing cycle.

But just as index investing drives stocks up in bull markets, it can accelerate their declines when sentiment shifts.

Once a market darling starts falling, fund outflows lead to more selling pressure, which triggers further index rebalancing. The current correction in CBA is exacerbated by this dynamic, and with more passive money still holding overweight positions, the forced selling isn’t done yet.

Where it stops, no one knows. But the super high valuation makes it a risky long play with this passive investing flow cycle, which is now beginning to exit the stock.

The Looming Refinancing War

Australia has just begun its interest rate cutting cycle, with a 25 basis point reduction in February 2025. Further falls are broadly expected this year.

Combined with historically high levels of mortgage stress, this could ignite another refinancing war in 2025 or 2026.

Recent data shows that over 1.5 million Australian households are experiencing mortgage stress, with delinquency rates creeping higher as borrowers struggle with high repayment burdens. Interest rate changes typically lead to a surge in refinancing activity as borrowers seek better deals, and this could set the stage for another aggressive competition among banks to retain and attract customers.

In such a scenario, CBA’s margins and market share could suffer. While it remains the dominant force in Australian banking, it is not immune to competitive pricing wars.

Smaller players like Macquarie (ASX: MQG) and ANZ (ASX: ANZ) have already demonstrated a willingness to undercut larger banks in pursuit of market share.

If another round of aggressive refinancing kicks off, CBA will be forced to sacrifice margin or risk losing volume. It’s like choosing between a punch to the gut or a slap to the face—either way, it’s not pretty.

Despite being the market leader, CBA remains vulnerable to the strategic decisions of its more nimble competitors, just as we’ve seen in previous pricing battles.

Better Market Leaders At Better Value

CBA is a strong company, but with low growth prospects. There are other ASX market leaders with stronger growth prospects and much more reasonable valuations.

CSL (ASX: CSL) is one such stock, one of the ASX’s most resilient and innovative companies, with a true unassailable edge. Compare this to banks, which are constantly at risk of being edged out by competitors and having to scrap it out for every dollar.

As a global leader in blood plasma therapies and vaccines, CSL operates in a niche market with significant barriers to entry. The company’s massive investment in research and development ensures a pipeline of new products that sustain its market dominance and pricing power.

CSL’s valuation reflects its premium status, but it continues to justify this through consistent earnings growth. It trades at a trailing PE ratio of 30x.

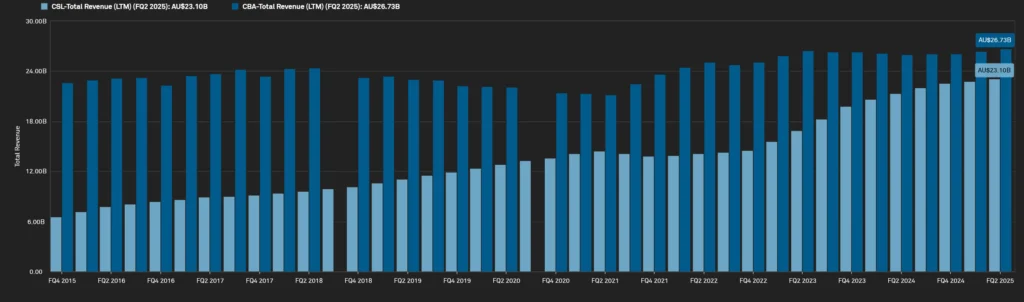

While that’s very similar to CBA, the growth story is worlds apart. As shown in the following chart, CSL has grown its revenue by 213% over the last decade, while CBA has eeked out a measly 15%.

At roughly the same PE valuation, CSL makes for a much more compelling case.

CSL and CBA LTM revenue by quarter (Source: S&P Capital IQ)

Unlike banks that are exposed to cyclical financial markets and credit risks, CSL benefits from a structural demand for its products, making it a more predictable and defensive investment.

While its dividend yield is lower than that of major banks, CSL focuses on reinvesting in growth, driving long-term capital appreciation. It has historically delivered strong shareholder returns through both earnings expansion and capital gains.

The nature of its business—a healthcare leader that provides life-saving treatments—ensures longevity and resilience.

Whereas banks can lose market share due to regulatory changes, fintech disruptions, or economic cycles, CSL’s competitive moat is fortified by its intellectual property, high barriers to entry, and continuous innovation.

Furthermore, its global footprint continues to expand, with growing demand for immunoglobulin therapies, influenza vaccines, and recombinant protein therapies positioning it for sustained growth over the next decade.

As healthcare needs grow worldwide, CSL stands as a great example of an ASX-listed company with a genuine long-term growth runway.₹

Mid-Cap Finance Stocks That Are a Better Bet

For those looking for opportunities in the financial sector, the mid-cap space offers far better value and growth potential than CBA:

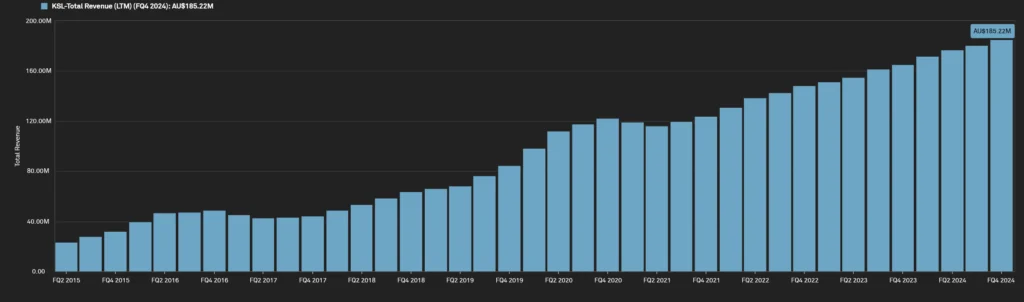

Kina Securities (ASX: KSL) is a unique play on the Papua New Guinea (PNG) banking sector, offering strong valuation metrics and growth potential. Unlike Australia’s saturated banking industry, PNG has a massive unbanked population, with financial services penetration still in its early stages.

KSL trades at a PE of 8.8x while delivering high earnings growth as it capitalises on the rising demand for banking, lending, and digital financial services in PNG. Revenue has grown by 598% over the last decade.

With improving infrastructure and increasing financial inclusion, Kina Securities is positioned to benefit from a rapidly expanding addressable market.

Investors should be warned that KSL’s healthy dividend yield of 7% attracts a 15% tax from the PNG government. On the plus side, the PNG is reducing the tax rate on KSL from 45% to 35%, which will provide a big boost to after-tax earnings.

KSL LTM revenue by quarter (Source: S&P Capital IQ)

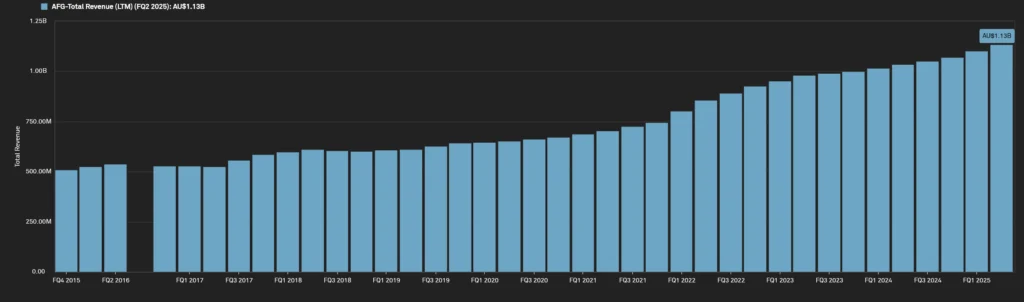

Australian Finance Group (ASX: AFG) is a market leader in its own segment as one of the largest mortgage broker networks in Australia.

A new refinancing war in the Australian mortgage market would be a significant tailwind for AFG, as the company generates revenue from the volume of loan lodgements.

Unlike the banks, which may see margin compression in a competitive environment, AFG benefits directly from increased mortgage activity. As more homeowners look to refinance for better deals, AFG is positioned to profit from the heightened transaction volume.

AFG has grown its revenue by 110% over the last decade. It’s PE currently stands at 15x. The trailing dividend yield is 4.84% and when grossed up for franking credits comes to 6.9%.

AFG LTM revenue by quarter (Source: S&P Capital IQ)

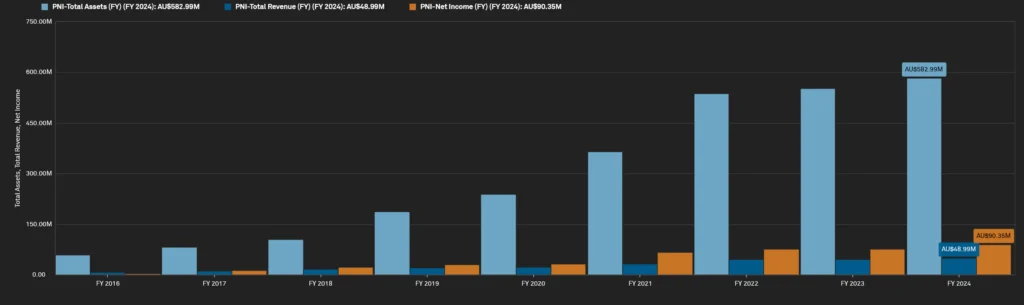

Pinnacle Investment Management (ASX: PNI) stands out as a powerhouse in the asset management industry, leveraging its multi-affiliate model to scale efficiently.

Unlike traditional financial institutions, PNI benefits from diversification across its investment firms, reducing reliance on any single asset class or strategy. The company's success is tied to funds under management (FUM) growth, which has been consistently strong due to investor demand for specialised strategies.

With ongoing structural shifts favouring independent asset managers over large banks, Pinnacle remains well-positioned for sustained growth.

Revenue has grown by 545% over the last decade. The PE ratio stands at 34x. The dividend yield is modest at 2.6%.

PNI assets, revenue and net income by year (Source: S&P Capital IQ)

The Illusion of Safety: Why 'Safe' Stocks Can Be the Riskiest

Investors often gravitate toward blue-chip stocks like CBA for their perceived stability. But sometimes, the stocks that look the safest are actually the most dangerous.

When everyone believes a stock can only go up, valuations detach from reality. CBA is the classic example. Investors treated it as a no-brainer defensive play, leading to relentless buying that pushed it to unsustainable levels. Now, as reality sets in, it’s worth being aware that even the biggest names can suffer steep declines when sentiment turns.

Be wary of overpaying for perceived 'safe' stocks. True investing safety lies in fundamentals, not in past performance or index weightings. CBA’s fall is a lesson in what happens when a stock becomes too popular for its own good—and this could be just the beginning of a much bigger downside to come.

If you’re still holding CBA, ask yourself this—do you really think a bank in a saturated market, with single-digit growth, deserves a tech stock valuation? The market doesn’t hand out free rides forever. Get ahead of the herd before reality sets in.

- ASX:CBA

- Banks

- Financials

- ASX:AFG

- ASX:CSL

- Healthcare

- Biotech

- ASX:PNI

- Valuation